Last Updated: February 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: November 2023

By: Danielle Burton

Category: Auto Refinancing

If your current car loan feels expensive, restrictive, or misaligned with your budget, you are not alone. Many Canadians are carrying high interest charges on their vehicle loans, locked into a loan agreement that no longer fits their financial goals. Whether your credit situation has improved, you are managing negative equity, or you simply want a better payment plan, it may be time to explore your options.

Refinancing a vehicle means replacing your current car loan with a new loan to lower your interest rate, reduce your monthly payment, or cut total interest costs. Unlike the trade-in process, auto loan refinancing allows you to keep your vehicle ownership intact while restructuring the financing attached to it. The auto loan refinancing process involves reviewing your credit, checking your loan terms for prepayment penalties, and submitting an application with a lender or online platform.

This guide explains how refinancing works in Canada, when it makes sense, what lenders review, and how a refinance loan can lower interest costs and improve your payment plan.

In This Guide:

- What Does It Mean to Refinance a Vehicle in Canada?

- When Should You Refinance?

- How Much Can You Save?

- How to Prepare Before Refinancing a Vehicle in Canada?

- How Does Seasonal Income Impact Eligibility?

- How to Refinance a Vehicle in Canada, Step by Step?

- What Hidden Fees Should You Watch For?

- Where in Canada Might Refinancing Be Limited?

- Is Refinancing a Vehicle in Canada Right for You?

- Conclusion

- Frequently Asked Questions

What Does It Mean to Refinance a Vehicle in Canada?

Refinancing a vehicle in Canada means restructuring your existing car loan rather than replacing your vehicle. Instead of going through the trade in process or buying a new car, you keep the same vehicle and change only the financing terms. The goal is to improve your loan based on your current financial situation, whether that means lowering your interest rate, reducing monthly payments, or adjusting the remaining term.

What typically changes are the financing terms, such as:

- Interest rate

- Monthly payment

- Remaining loan term

How the Auto Loan Refinancing Process Works in Canada

The process typically follows these steps:

- A lender reviews your credit profile, income, vehicle details, and remaining loan balance.

- If approved, the new lender issues funds to pay off your current auto loan.

- Your previous loan is closed.

- You begin payments under the new loan agreement.

There is no vehicle trade in involved when refinancing. You keep your current vehicle, and ownership remains the same throughout the process. The only change is to the loan agreement itself, which may include a new interest rate, adjusted loan term, or revised monthly payment structure based on your updated financial situation and lender approval terms.

What Refinancing Is Not

Refinancing does not mean:

- Trading in your car

- Automatically extending your loan

- Taking on additional debt

- Getting approved without qualification

It simply replaces one auto loan with another, ideally on more favourable terms.

Is Refinancing the Same as Debt Consolidation?

No. Vehicle refinancing replaces one existing auto loan with a new loan on the same vehicle. Debt consolidation, on the other hand, combines multiple debts such as credit cards, personal loans, or other obligations into a single new loan. The purpose of refinancing is to improve the terms of your current car loan, often through a lower interest rate or adjusted payment plan. If your goal is to reduce your monthly car payment or lower interest charges, refinancing your vehicle is the more direct and targeted solution.

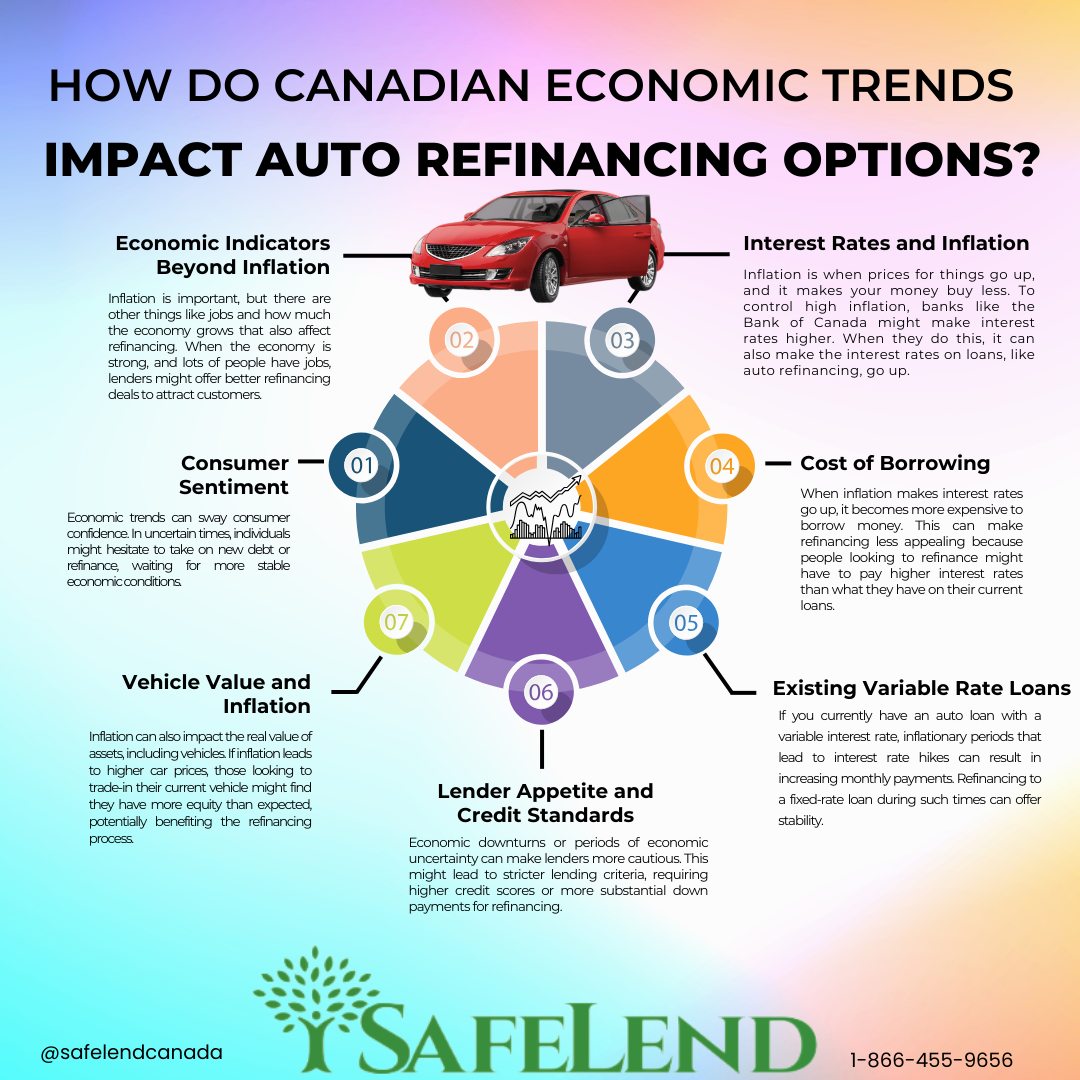

When Should You Refinance Your Car Loan in Canada?

Refinancing makes the most sense when your financial situation or market conditions have improved since you first secured your loan. Changes such as a stronger credit profile, increased income, or lower overall lending rates can create new opportunities. The goal is simple: secure a lower interest rate, reduce your monthly payment, or adjust your loan term so it better aligns with your current budget and long term financial plans.

Here are the most common situations where refinancing may be worth exploring.

1. Your Credit Score Has Improved

If your credit score has increased since you originally financed your vehicle, you may now qualify for a lower interest rate.

Even a moderate credit improvement can reduce your interest rate by several percentage points, depending on lender guidelines and your overall financial profile. A lower rate decreases the amount of interest charged over the life of the loan, which can translate into hundreds or even thousands of dollars in long term savings. Over time, those savings can meaningfully improve your overall borrowing costs and financial flexibility.

2. Interest Rates Have Dropped

If you financed your vehicle during a period of higher lending rates, you may be able to refinance into a lower rate environment.

Market shifts can create refinancing opportunities, especially if your current loan was secured at double digit interest.

3. Your Income Has Increased

If your income has grown or your employment has stabilized, lenders may now view you as a lower risk borrower.

Improved income can increase approval chances and may help you qualify for better loan terms.

4. You Want to Lower Your Monthly Car Payment

Refinancing can reduce your payment in two ways:

- Securing a lower interest rate

- Extending the remaining loan term

Lowering your monthly obligation can improve cash flow and reduce pressure on your overall debt service ratio.

This can be especially helpful if you are preparing for a major financial milestone such as applying for a mortgage.

5. You Have at Least 12 to 24 Months Remaining on Your Loan

Refinancing works best when there is enough time left on your loan to benefit from interest savings.

If your loan is nearly paid off, the savings may not outweigh potential fees or administrative costs.

When Refinancing May Not Make Sense

Refinancing may not be ideal if:

- Your vehicle has very high mileage

- Your loan balance exceeds your vehicle value significantly

- You are close to paying off the loan

- The new rate is not meaningfully lower than your current rate

Always compare total interest costs, not just monthly payment.

Quick Rule of Thumb

If you can reduce your interest rate by 1 to 2 percentage points or more, refinancing is often worth reviewing.

The larger the loan balance and the longer the remaining term, the greater the potential savings.

How Do You Know for Sure?

The best way to determine whether refinancing makes sense is to review:

- Your current interest rate

- Your remaining balance

- Your credit profile

- Current Canadian auto lending rates

A simple refinance review can clarify your potential savings without requiring you to commit immediately.

How Much Can You Save by Refinancing a Vehicle in Canada?

The amount you can save by refinancing depends primarily on three factors:

- Your current interest rate

- Your remaining loan balance

- Your remaining loan term

Even a small interest rate reduction can lead to meaningful savings over time, especially when the remaining balance is high and the term is long.

Example: Interest Rate Reduction Scenario

Below is a simplified comparison showing how refinancing can reduce interest costs while keeping the same remaining term.

| Current Loan | Refinanced Loan | |

|---|---|---|

| Balance | $30,000 | $30,000 |

| Interest Rate | 10.9% | 7.4% |

| Remaining Term | 60 months | 60 months |

| Monthly Payment | ~$652 | ~$601 |

| Monthly Savings | — | ~$51 |

| Total Interest Savings | — | $3,000+ |

In this example, the borrower keeps the same term but secures a lower interest rate. The reduced rate lowers the monthly payment and decreases total interest paid over the life of the loan.

Example: Lower Monthly Payment Strategy

Some borrowers choose to extend the loan term to reduce their monthly obligation.

| Current Loan | Refinanced Loan | |

|---|---|---|

| Loan Balance | $25,000 | $25,000 |

| Interest Rate | 11.5% | 8.0% |

| Remaining Term | 48 months | 60 months |

| Estimated Monthly Payment | Higher | $100+ Lower |

Estimated Monthly Payment Reduction: Over $100

Extending the loan term can lower your monthly payment and improve short term cash flow. However, because repayment is spread over a longer period, total interest paid over time may increase. This strategy can make sense if immediate budget relief is a priority, but it should be weighed against long term borrowing costs.

How to Evaluate Your Potential Savings

When reviewing a refinance offer, compare:

- Total projected interest cost

- Monthly payment impact

- Remaining term length

- Any applicable fees

The goal is not just a lower payment, but a loan structure that improves your overall financial position.

When evaluating refinancing, always compare total interest costs — not just the monthly payment. A longer term may lower your payment but increase what you pay overall.

How to Prepare Before Refinancing a Vehicle in Canada

Before starting the application process, it helps to prepare your information and understand your current car loan details. Taking a few practical steps in advance can make the auto refinancing process smoother and help you determine whether a new refinance loan will truly improve your financial position.

Review Your Current Loan Agreement

Begin by reviewing your existing car loan documents.

Confirm:

- Your remaining balance

- Current interest rate

- Remaining term

- Monthly payment amount

- Whether prepayment penalties apply

Understanding these details allows you to compare any auto refinance offer accurately and determine whether the new loan structure reduces interest charges or addresses concerns like negative equity.

Review Your Credit Profile

While there is no universal minimum credit score required, it is helpful to review your credit history before applying. Checking for reporting errors or recent changes can help you understand how lenders may evaluate your refinance loan request.

If your financial situation has improved since you first secured your car loan, refinancing may offer better terms.

Estimate Your Potential Savings

Before submitting a refinance application, estimate how much you could realistically save.

Consider:

- The difference between your current rate and potential new rate

- Monthly payment impact

- Total projected interest cost

- Any applicable fees

The goal of auto refinancing is not just to lower payments, but to improve the overall structure of your vehicle financing.

Gather Required Documentation

Most refinance applications require:

- Proof of income

- Government issued identification

- Current loan statement

- Vehicle information

If you have seasonal employment or variable income, you may need additional documentation, such as tax returns or deposit history, to demonstrate income consistency.

Confirm Vehicle Eligibility and Ownership

Refinancing allows you to keep your current vehicle. Your vehicle ownership does not change.

However, lenders may review:

- Vehicle age

- Mileage

- Condition

- Remaining balance compared to value

Understanding these factors in advance can help you set realistic expectations before submitting a refinance loan application.

Clarify Your Financial Objective

Finally, determine your goal.

Are you looking to:

- Lower your monthly payment

- Reduce overall interest charges

- Address negative equity

- Improve short term cash flow

- Strengthen your broader financial plan

Being clear about your objective helps you evaluate auto refinance offers more effectively.

Preparing in advance helps you approach refinancing a vehicle with confidence. When you understand your current car loan, review your credit history, gather documentation, and clarify your goals, the application process becomes more straightforward and strategic.

How Does Seasonal Employment or Irregular Income Affect Vehicle Refinancing Eligibility?

Seasonal or irregular income does not automatically prevent you from refinancing in Canada. Lenders understand that earnings can fluctuate during the year and focus more on overall income consistency and proper documentation than on perfectly steady pay periods. If your income pattern is predictable and supported by tax returns, bank statements, or deposit history, you may still qualify for refinancing options.

If you work seasonally or earn commission based income, lenders may review:

- Income history over 12 to 24 months

- Year over year consistency

- Average monthly earnings

- Tax returns or bank statements

Debt ratios are often calculated using your average monthly income rather than your highest earning months. This allows lenders to assess whether your payment plan remains affordable during slower income periods throughout the year. Showing consistent deposits, stable income patterns, and a strong vehicle payment history can strengthen your refinance application and reduce the lender's perceived risk when reviewing your file.

If your income pattern is established and verifiable, refinancing may still be available.

How to Refinance a Vehicle in Canada, Step by Step

Refinancing is a structured but straightforward process.

Step 1. Review Your Current Loan

Gather:

- Remaining balance

- Interest rate

- Monthly payment

- Remaining term

- Vehicle details

Step 2. Compare Refinancing Options

In Canada, borrowers typically refinance through either a dealership or an online platform.

Dealership refinancing:

- Often tied to limited lender relationships

- May focus on vehicle transactions

- Rate comparison can be restricted

Online platforms like SafeLend Canada:

- Work with multiple licensed Canadian lending partners

- Focus specifically on refinancing existing auto loans

- Provide digital application and comparison process

- You keep your vehicle and only change your loan

SafeLend operates as an affiliate platform, facilitating loan placement based on your credit profile and financial situation.

Step 3. Submit Documentation

You may need:

- Proof of income

- Identification

- Current loan statement

- Vehicle information

Step 4. Approval and Payoff

If approved, the new lender issues funds directly to your current lender to pay off the remaining balance on your auto loan. Once the payoff is processed, your previous loan is officially closed and reported as satisfied. You then begin making payments under the new refinance agreement according to the updated interest rate and payment schedule. From the borrower's perspective, the vehicle remains the same, but the financing terms and monthly obligation are adjusted.

Depending on who you've chosen to work with, approvals can take several days to a few weeks depending on documentation and lender processing.

What Hidden Fees Should You Watch for When Refinancing a Vehicle in Canada?

While refinancing can create savings, it is important to understand potential costs.

Common fees include:

Early Repayment Penalties

Some loans include prepayment clauses. Review your current agreement before refinancing.

Origination or Processing Fees

Some lenders charge a one time fee to issue the new loan.

Lien Registration Fees

Switching lenders requires registering a new lien on your vehicle. Costs vary by province.

Administrative Fees

These may include document preparation or credit report processing.

Appraisal or Inspection Fees

Some lenders require vehicle inspections, especially in non prime scenarios.

Variable Rate Risk

If the rate is variable, payments may increase over time.

Insurance Requirements for Auto Loan Refinancing in Canada

Some lenders require specific coverage levels, which may affect your monthly costs.

Always compare total interest savings against all fees to determine whether refinancing improves your financial position.

Where in Canada Might Refinancing Be Limited?

Refinancing a vehicle in Canada is widely available, but access can vary depending on your province or territory. Differences in legal frameworks, lender licensing, and regional infrastructure can affect which refinance loan options are offered in certain areas. While many Canadians can secure competitive auto refinancing rates, understanding regional limitations helps set realistic expectations before starting the application process.

Quebec's Distinct Legal Framework: Quebec operates under its own civil code and consumer protection regulations, which differ from other provinces. As a result, some online refinancing platforms and lenders may not currently operate in Quebec, or they may structure refinance loans differently. Borrowers in Quebec may find fewer traditional auto loan refinancing options compared to other provinces and may need to work directly with financial institutions licensed within the province.

Although lending markets continue to evolve, eligibility and lender participation in Quebec can differ from the rest of Canada.

The Northern Territories: In Yukon, Northwest Territories, and Nunavut, access to vehicle refinancing may be more limited due to smaller lender networks and logistical considerations. Infrastructure, vehicle transport realities, and regional servicing limitations can affect lender participation. Borrowers in these territories may have fewer refinancing options available, particularly in non prime or subprime scenarios.

While options may exist, availability can vary more significantly than in larger provinces.

Documentation Requirements: Regardless of your location, refinancing a vehicle requires documentation. However, requirements can vary slightly by province. Lenders may request proof of income, vehicle ownership details, loan statements, or residency documentation. Registration processes and lien handling procedures can also differ depending on provincial regulations.

Understanding your province's documentation requirements in advance can help avoid delays during the refinance application process.

SafeLend Canada Availability

SafeLend currently operates in select provinces and partners with licensed Canadian lenders. Availability depends on provincial regulations and lender participation. If your province is not eligible, you may need to explore alternative local lenders, banks, or credit unions that are authorized to offer vehicle refinancing services in your region.

Why Regional Awareness Matters

Most Canadians can access refinance loan opportunities to lower their car loan interest rate, reduce monthly payments, or address negative equity. However, refinancing availability is not identical across all provinces and territories. Understanding your regional lending landscape allows you to approach auto refinancing with clarity and realistic expectations.

Whether you are located in Quebec, the northern territories, or another province, knowing the regulatory environment and lender participation levels can help you navigate the refinancing process with greater confidence.

Is Refinancing a Vehicle in Canada Right for You?

Refinancing a vehicle can be a smart financial move when it clearly improves your loan structure. The decision should be based on measurable outcomes, not just the idea of changing lenders.

Refinancing may make sense if it:

- Lowers your monthly payment

- Reduces total interest charges

- Improves short term cash flow

- Helps manage negative equity

- Aligns better with your current financial goals

A refinance loan does not replace your vehicle or change ownership. It simply restructures the financing attached to your car loan. When done properly, it can strengthen your overall financial position without increasing debt.

However, refinancing is not always the right choice. If the interest rate reduction is minimal, the remaining term is short, or the total cost savings are limited after fees, the benefit may not justify the change.

The most important question is simple:

Will refinancing meaningfully improve your financial situation?

If the answer is yes, reviewing your options may be worthwhile. If the benefit is unclear, comparing total costs before moving forward is essential.

Refinancing a vehicle should support your broader financial strategy, not complicate it.

Conclusion: Refinancing a Vehicle in Canada with Confidence

Refinancing a vehicle in Canada can lower your monthly payment, reduce overall interest costs, and improve your financial flexibility. If you are carrying high interest vehicle loans, managing negative equity, or have improved your credit, refinancing may help you secure a lower rate and create a more manageable payment plan, all while keeping your current vehicle.

The key is understanding:

- How the auto loan refinancing process works

- What realistic savings a refinance loan can deliver

- Whether prepayment penalties exist in your current loan agreement

- What fees or interest charges may apply

- How your credit history affects eligibility

- Whether the new car loan strengthens your long term financial position

Not every borrower will benefit equally from refinancing. Approval and savings depend on your credit, remaining balance, current interest rate, income stability, and how the refinance application is set up. Some borrowers may qualify for a meaningful interest rate decrease, while others may see only modest changes based on lender guidelines and vehicle eligibility. Unlike the trade-in process, refinancing focuses solely on improving the financing terms attached to your current vehicle, not replacing the vehicle itself.

When an interest rate decrease is meaningful and the new terms align with your financial goals, auto refinancing can be a strategic way to regain control of your car loan.

Taking time to review your options, compare lenders, and fully understand the refinancing process and total costs allows you to move forward with clarity, confidence, and a stronger financial foundation.

Frequently Asked Questions (FAQ) on Vehicle Refinancing in Canada

What does it mean to refinance a vehicle in Canada?

Refinancing a vehicle in Canada means replacing your current auto loan with a new loan, ideally with a lower interest rate, a lower monthly payment, or a better term. The new lender pays off your existing loan, and you make payments under the new agreement.

When should you refinance your car loan in Canada?

Refinancing is often worth reviewing if your credit score has improved, your income is more stable, you are paying a high interest rate, or you want a lower monthly payment. It also helps when you still have at least 12 to 24 months left on your loan.

How much can you save by refinancing a vehicle?

Savings depend on your current rate, remaining balance, and term. A lower rate can reduce both your monthly payment and total interest, while a longer term can reduce your monthly payment but may increase total interest over time.

Does refinancing a vehicle hurt your credit score?

Refinancing may involve a credit inquiry, which can cause a small, temporary dip. If refinancing helps you manage payments more consistently, it can support stronger credit health over time.

Can you refinance a vehicle in Canada with bad credit?

Yes, refinancing may still be possible with fair or challenged credit, depending on income, payment history, vehicle details, and lender guidelines. Consistent on time auto payments can strengthen your application.

How does seasonal employment or irregular income affect refinancing eligibility?

Seasonal or irregular income does not automatically prevent you from qualifying. Lenders usually look for predictable, verifiable income history, often based on 12 to 24 months of records, plus stable deposits and manageable debt ratios.

What fees should you watch for before refinancing a vehicle in Canada?

Common costs can include lien registration fees, administrative or processing fees, possible appraisal or inspection fees, and in some cases origination fees. You should also confirm whether your current loan has any early repayment penalties, and whether the new rate is fixed or variable.

Where in Canada can vehicle refinancing be more limited?

Availability can vary by province and territory due to differences in lender licensing, legal frameworks, and infrastructure. Quebec and the northern territories can have fewer options with some online platforms, so it is best to confirm eligibility before applying.

Is it better to refinance through a dealership or an online platform?

A dealership may be convenient but is often tied to limited lender relationships and may prioritize vehicle transactions. An online platform focused on refinancing can help you compare options across lending partners, depending on your province and eligibility.

Can I get a quote before my credit is formally reviewed?

In eligible provinces, some platforms offer a free quote option that estimates potential savings before a formal credit review. This helps you understand possible outcomes before moving forward with a full application.

"At SafeLend Canada, we believe that refinancing your vehicle can be a game-changer for your financial well-being. It's not just about lowering your monthly payments or reducing interest rates; it's about taking control of your financial future and driving towards a brighter tomorrow."

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.