Last Updated: April 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: June 2023

By: Danielle Burton

Category: Negative Equity, Credit, Auto Refinancing, Trade in

Refinancing your auto loan in Canada can be one of the simplest ways to lower your interest rates, reduce your monthly car payments, and take back control of your finances. If your current vehicle loan feels too expensive or tied to high-interest rates from when you first secured your automobile financing, you are not stuck with it.

Many Canadians don’t realize they can replace their current loan with better terms based on their credit, payment history, and financial situation. By reviewing your credit reports and exploring new options, you may qualify for improved terms that better reflect where you are today. Whether your credit score has improved or interest rates have shifted, refinancing can create real savings over time and even help address challenges like negative equity.

In this guide, you’ll learn how the refinancing process works, when it makes sense to move beyond dealership financing, and how SafeLend Canada can help you explore better options.

Auto loan refinancing in Canada means replacing your current car loan with a new one that offers better terms based on your current financial situation.

Road Map:

- 1. Why Your Current Car Loan Might Be Costing You More Than You Think

- 2. Chop My Rate: A Smarter Way to Lower Your Car Loan Payments in Canada

- 3. What Actually Happens When You Refinance a Car Loan?

- 4. The Smart Way to Lower Your Car Payment Without Trading In Your Vehicle

- 5. SafeLend Canada vs Dealership Financing: What’s the Real Difference?

- 6. Will Refinancing Impact Your Credit, or Help It?

- 7. Can You Refinance a Car Loan with Bad Credit? Here’s What to Know

- 8. Where Most People Go Wrong with Auto Loan Refinancing

- 9. Final Thoughts: Is It Time to Rethink Your Car Loan?

- 10. Frequently Asked Questions About Auto Refinancing

Why Your Current Car Loan Might Be Costing You More Than You Think

Your current car loan may be costing you more than necessary if your interest rate, loan terms, or financial situation no longer reflect today’s conditions. Many Canadians lock in a loan at the time of purchase and never revisit it, even when better options become available.

Over time, several factors can quietly increase the cost of your vehicle loan. Common reasons include:

Being locked into high-interest rates

If your loan was approved when your credit profile was weaker, you may still be paying more interest than necessary today.

Changes in your financial situation

Improvements in your income, reduced debt, or stronger payment history may now qualify you for better interest rates and loan terms.

Outdated loan terms

Your current automobile financing may no longer align with your financial goals, especially if your budget or priorities have changed.

Vehicle depreciation over time

As your car’s value decreases, your loan may become misaligned, potentially leading to challenges like negative equity.

Even a small difference in interest rates can add up to hundreds or thousands of dollars over the life of your loan. Without revisiting your options, you could be leaving meaningful savings on the table.

The key takeaway is simple: your car loan is not something you have to keep unchanged for its full term. If your current loan feels expensive, restrictive, or out of sync with your financial goals, it may be time to explore a better option.

“We simply find you a lender ready to offer you a lower rate, repay your previous car loan, cancel all its obligations, and you get to save money!” ~ SafeLend Canada

Chop My Rate: A Smarter Way to Lower Your Car Loan Payments in Canada

“Chop My Rate” is a simple way to describe auto loan refinancing in Canada, where you replace your current car loan with a new one that offers better terms based on your current financial profile. The goal is to reduce your interest rate, lower your monthly payments, or improve how your loan fits your budget.

Instead of staying locked into a loan that no longer works for you, refinancing gives you the opportunity to reset your financing. This can be especially valuable if your credit score has improved, interest rates have changed, or your financial situation is stronger than when you first secured your loan.

Lowering your interest rate is one of the most effective ways to reduce the overall cost of your vehicle. Even a small decrease can lead to meaningful savings over time. In some cases, borrowers also choose to adjust their loan term, which can help lower monthly payments and improve cash flow, depending on their financial goals.

Refinancing is not just about reducing payments, it is about creating a loan structure that better supports your current lifestyle. Whether your focus is saving money, improving flexibility, or gaining more control over your finances, the right refinance strategy can help you move forward with confidence.

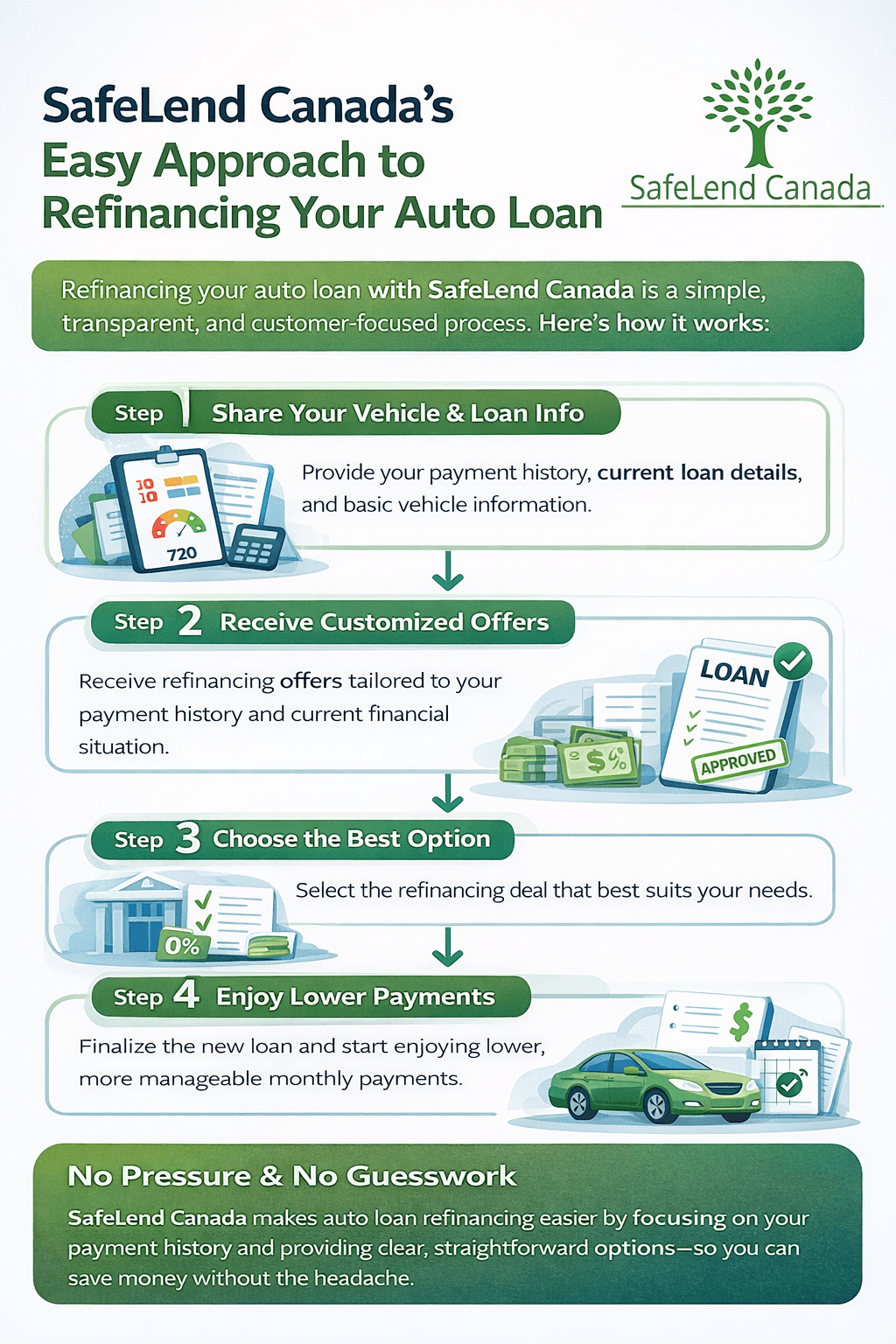

What Actually Happens When You Refinance a Car Loan?

Refinancing a car loan is a straightforward process where your existing loan is replaced with a new one that offers better terms. Instead of continuing with your current lender, a new lender pays off your remaining loan balance, and you begin making payments under the new agreement.

The process typically starts with reviewing your current loan details, including your remaining balance, interest rate, and monthly payments. From there, you can explore refinancing options based on your credit profile, income, and the value of your vehicle.

Once you submit a refinance application, lenders assess your information to determine what terms you qualify for. This may include a lower interest rate, adjusted loan term, or a different payment structure that better fits your financial situation.

If you move forward with an offer, the new lender pays out your existing loan directly. This closes your original loan, and your new loan begins with updated terms and payments.

The key advantage is that you keep your current vehicle while improving the structure of your loan. There is no need to sell or trade in your car, making refinancing a simple way to adjust your financing without starting over.

Here’s a simple breakdown of how the refinancing process works:

The Smart Way to Lower Your Car Payment Without Trading In Your Vehicle

Many drivers assume that the only way to lower their car payment is to trade in their vehicle and start over with a new loan. In reality, auto loan refinancing offers a simpler and often more cost-effective solution.

By refinancing your existing car loan, you can adjust your interest rate, loan term, or overall structure without giving up the vehicle you already own. This allows you to reduce your monthly payments while avoiding the added costs that can come with trading in, such as dealer markups, new financing fees, or rolling negative equity into a new loan.

For borrowers who are happy with their current vehicle, refinancing keeps things straightforward. Instead of restarting the buying process, you are improving the loan you already have. This can be especially valuable if your financial situation has improved or if better lending options are now available.

Refinancing also gives you more control over your financial strategy. Whether your goal is to improve cash flow or reduce the total cost of your loan, adjusting your current financing can often achieve those results without the complexity of replacing your vehicle.

For many Canadians, refinancing is one of the easiest ways to improve their car loan without taking on the risks or costs of a new vehicle purchase.

SafeLend Canada vs Dealership Financing: What’s the Real Difference?

When exploring your refinancing options, it’s important to understand how different approaches compare. Many borrowers default to dealership financing out of convenience, but the experience and outcomes can vary significantly.

Here’s how SafeLend Canada compares to traditional dealership financing in terms of transparency, flexibility, and overall experience.

| Category | SafeLend Canada | Some Car Dealerships |

|---|---|---|

| Loan Process | Simple, transparent, and easy to understand | Can be complex and less transparent |

| Customer Experience | Focused on long-term relationships and support | Often transactional and short-term focused |

| Refinancing Focus | Helps lower high-interest rates on existing vehicle loans | May prioritize new automobile financing and trade-ins |

| Comfort & Discretion | Private, secure, and pressure-free process | Customers may feel pressured into decisions |

| Loan Applications | Typically a streamlined loan application process | May submit multiple applications (“shotgunning”), which can impact credit reports |

| Understanding Your Options | Clear breakdown of all available refinancing options | Options may not always be fully explained |

For many Canadians, the difference comes down to control, transparency, and the ability to choose a refinancing solution that truly fits their financial situation.

Will Refinancing Impact Your Credit, or Help It?

Refinancing a car loan may cause a small, temporary impact on your credit score, but in many cases, it can also help improve your credit over time when managed responsibly.

When you apply to refinance, lenders perform a hard credit inquiry to assess your eligibility. This can result in a slight, short-term decrease in your score. However, this impact is typically minimal and does not last long, especially if you continue to make consistent, on-time payments.

The long-term effect of refinancing often depends on how your new loan is structured and how you manage it. If refinancing helps you secure a lower monthly payment, it can make it easier to stay on track and avoid missed payments, which is one of the most important factors in building or maintaining a strong credit profile.

In some cases, refinancing may also improve your overall debt management by better aligning your loan with your financial situation. This can contribute to healthier credit habits over time, especially if it reduces financial strain.

The key takeaway is that refinancing is not something to fear from a credit perspective. When done for the right reasons and managed properly, it can be a step toward improving both your financial position and your credit health.

Many lenders, including platforms like SafeLend Canada, may start with a soft credit check, allowing you to explore your options without impacting your score.

Can You Refinance a Car Loan with Bad Credit? Here’s What to Know

Yes, you can refinance a car loan with bad credit in Canada.. Your options may be more limited than prime borrowers, but there are still lenders who work with non-prime credit, especially if you’re dealing with high-interest rates.

What Do Lenders Look at Beyond Your Credit Score?

Your eligibility will depend on several factors beyond just your credit score. Lenders may look at your income, payment history, credit, remaining loan balance, and your vehicle’s value. If you have been making consistent payments or your financial situation has improved, you may still qualify for better interest rates or more flexible terms through the refinancing process.

What Can Refinancing Actually Improve?

Refinancing with bad credit does not always guarantee a significantly lower rate, but it can still provide meaningful benefits. Some borrowers are able to reduce their monthly payments, adjust their loan term, or restructure their loan application in a way that makes their vehicle loans more manageable. In certain cases, refinancing can also help address challenges like negative equity while creating an opportunity to rebuild credit through consistent, on-time payments.

How Can You Find the Right Refinancing Option?

It is important to compare multiple options rather than relying solely on dealership financing or accepting the first offer. Different lenders have different approval criteria, and exploring a range of solutions can help you find a refinancing option that better fits your situation. Platforms like SafeLend Canada can simplify this process by connecting you with multiple lenders and helping you review your options in one place.

Where Most People Go Wrong with Auto Loan Refinancing

Auto loan refinancing can be a powerful financial tool, but only when the refinancing process is approached with a clear understanding of the details. Many borrowers miss out on the full benefits by focusing on the wrong factors or rushing their loan application without fully exploring their options.

Avoiding these common mistakes can help you get the most out of the refinancing process:

- Focusing only on the monthly payment: Lower payments can improve cash flow, but extending your loan term too far may increase the total interest paid over time, especially if you are still dealing with high-interest rates.

- Not comparing multiple offers: Lenders evaluate applications differently based on your credit reports and payment history, which means interest rates and terms can vary significantly.

- Overlooking key loan details: Missing factors like prepayment penalties, remaining balance, or negative equity can lead to unexpected costs when refinancing your automobile financing.

- Applying too early in the process: If your financial situation or credit profile has not improved, your refinancing options may be limited.

- Relying only on dealership financing: Dealerships may prioritize convenience over flexibility, while exploring multiple lenders can often lead to better long-term outcomes.

Taking the time to review your options, including alternatives to dealership financing, can lead to better long-term results. Platforms like SafeLend Canada can help simplify this process by allowing you to compare multiple options in one place.

Final Thoughts: Is It Time to Rethink Your Car Loan?

Your car loan should support your financial goals, not work against them. If your current vehicle loan feels expensive or no longer fits your situation, especially if it’s tied to high-interest rates from your original automobile financing, it may be time to explore better options.

Auto loan refinancing in Canada gives you the opportunity to adjust your loan based on where you are today, not where you were when you first applied through a financial institution. By reviewing your credit reports, payment history, and key loan details like your remaining balance and vehicle details, you may qualify for lower interest rates and more flexible terms. This can be especially important if you are dealing with challenges like negative equity or a loan structure that no longer fits your needs.

The key is to approach the refinancing process with clarity. Understanding your current loan, including any prepayment penalties, and exploring options beyond dealership financing or the traditional trade-in process can help you identify the best potential solutions for your situation.

If you are ready to see what your options look like, taking the first step can be simpler than you might expect. Platforms like SafeLend Canada make it easy to complete a refinance application, compare options across different vehicle loans, and find a solution that helps lower your car payments and better align with your financial strategy.

Frequently Asked Questions About Auto Refinancing

What does it mean to “chop your rate” on a car loan?

“Chop your rate” means refinancing your car loan to secure a lower interest rate or better terms. This can help reduce your monthly payments and the total cost of your loan over time.

How does refinancing a car loan actually work?

Refinancing replaces your existing car loan with a new one. The new lender pays off your current loan, and you begin making payments under new terms that may better fit your financial situation.

Can I refinance my car loan with bad credit in Canada?

Yes, refinancing is possible with bad credit. Lenders may also consider your income, payment history, and vehicle value when reviewing your application, not just your credit score.

Will refinancing a car loan affect my credit score?

Refinancing may cause a small, temporary drop in your credit score due to a credit check. However, making consistent, on-time payments on your new loan can help improve your credit over time.

When is the best time to refinance a car loan?

The best time to refinance is when your credit score has improved, interest rates have dropped, or your financial situation has become more stable. These factors can help you qualify for better loan terms.

Can refinancing lower my monthly car payment?

Yes, refinancing can lower your monthly car payment by securing a lower interest rate or adjusting your loan term. It is important to consider both your monthly savings and the total cost of the loan.

Do I need to trade in my car to refinance my loan?

No, refinancing allows you to keep your current vehicle. Your existing loan is replaced with a new one, without the need to trade in or purchase a new car.

What should I watch out for when refinancing a car loan?

Common mistakes include focusing only on monthly payments, not comparing multiple offers, and overlooking total loan costs or fees. Reviewing all terms carefully helps you make a better decision.

It puts a smile on our faces to see you save money so you can spend it on things way more fun and meaningful than high-interest rates! Why pay more than you have to? ~ SafeLend Canada

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.