Last Updated: April 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: November 2024

By: Danielle Burton

Category: Auto Refinance, Negative Equity, Trade-In

If you are wondering, can you refinance your car loan in Canada, the answer is yes, but the better question is whether it is the right move for your situation right now.

Auto loan refinancing can help lower your monthly car payments, reduce your interest rate, or adjust your loan terms, but the results depend on more than just applying. Factors such as your credit history, current loan balance, vehicle equity, and overall financial health all play a role in determining the loan options available to you.

As part of the auto loan refinance process, lenders may review your credit report, credit scores, income stability, and existing financial obligations to better understand your situation. These details influence not only your approval, but also your potential for interest savings, improved cash flow, and greater financial flexibility.

Many Canadians also have more specific questions beyond the basics, such as whether you can refinance more than once, how refinancing affects your credit rating, or whether it makes sense if you have negative or positive equity.

Understanding these factors can help you make more informed financial decisions before starting your refinance application.

This guide breaks down those real-world scenarios while also walking you through how the application process works with SafeLend Canada. The goal is to help you understand not just how to refinance your loan, but when it makes sense and what to expect before moving forward.

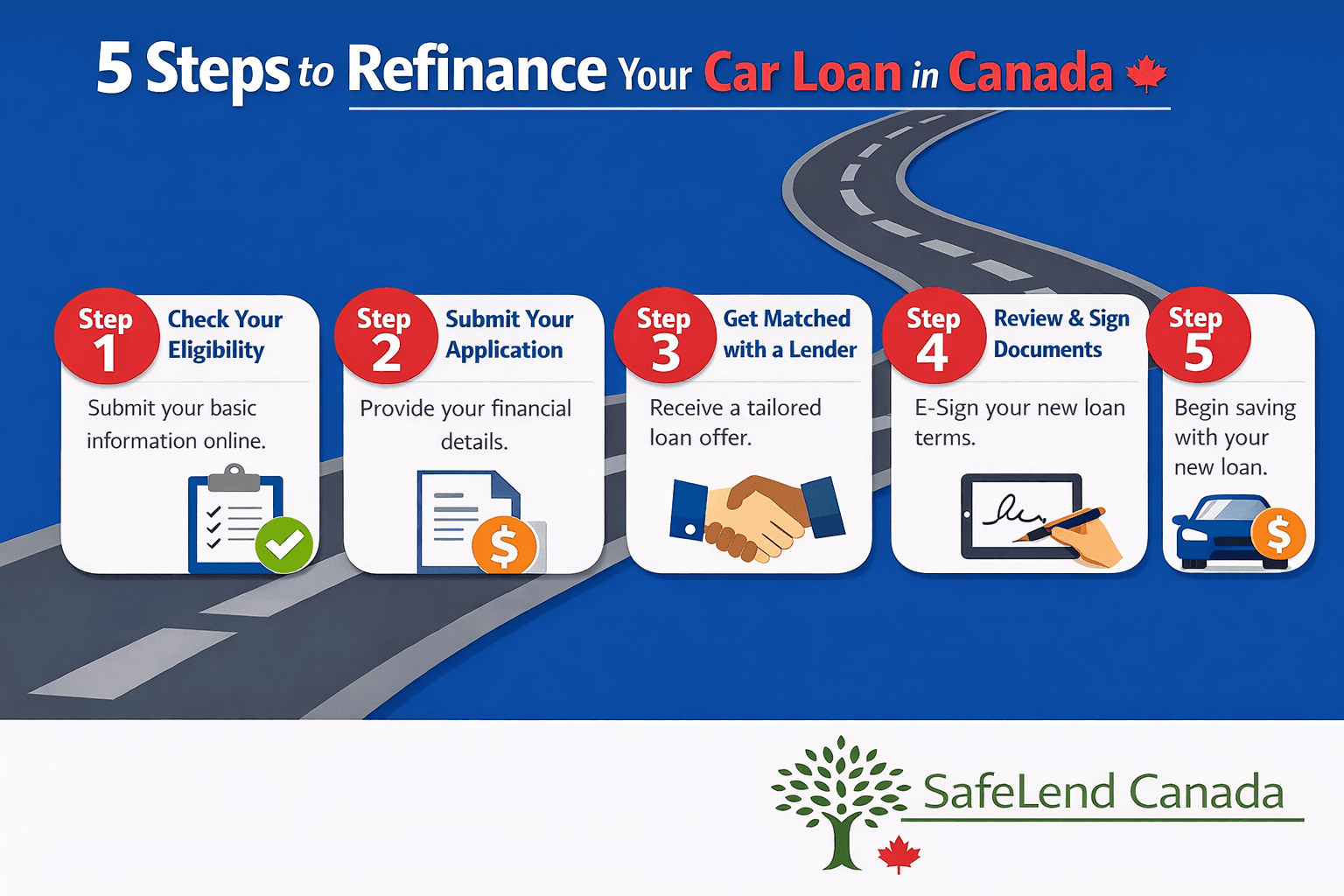

Step-by-Step Refinancing Process

- Step 1: Is Refinancing Your Car Loan the Right Move for You in Canada?

- Step 2: Complete Your Auto Loan Refinancing Application

- Step 3: Get Matched with the Right Lender for Your Situation

- Step 4: Review and Sign Your Refinancing Documents

- Step 5: Transition to Your New Loan and Start Saving

Key Questions Answered

Step 1: Is Refinancing Your Car Loan the Right Move for You in Canada?

Refinancing your car loan can be a smart financial move, but it is not the right solution for every situation. The goal is not simply to refinance your loan, it is to improve your overall financial health based on where you stand today.

When Auto Loan Refinancing Makes Sense

In Canada, auto loan refinancing typically makes the most sense when you can secure a lower interest rate, reduce your monthly car payments, or adjust your loan terms to better match your budget. This often applies if your credit history has improved, your income has stabilized, or your financial obligations have changed since you first arranged your vehicle financing.

You may want to consider refinancing if you are looking to:

- Lower your interest rate and reduce overall interest costs

- Reduce your monthly payments to improve cash flow

- Increase financial flexibility with better loan terms

- Restructure your loan to better match your current situation

What to Watch Out for Before Refinancing

It is important to look beyond just the monthly payment. While extending your loan term can reduce your payments, it may also increase the total interest paid over time.

Other factors that may impact your loan options include:

- Vehicle depreciation

- Limited vehicle equity

- A high remaining loan balance

How to Evaluate Your Current Loan Position

Before moving forward, review your current loan details, including your interest rate, remaining balance, and payment structure. Looking at your credit report, credit rating, and overall financial position can help you better understand what lenders will consider during the refinance application process.

Think about what you want to improve:

- Lower overall costs

- Better monthly cash flow

- More flexibility in your loan structure

If the numbers make sense, an auto loan refinance can help you regain control of your payments and better align your financing with your current financial needs. Understanding your current position is the most important first step in the process.

Step 2: Complete Your Auto Loan Refinancing Application

Once you have decided that refinancing makes sense for your situation, the next step is completing your refinance application. With SafeLend Canada, this application process is designed to be simple, secure, and fully online, allowing you to explore your auto loan refinancing options from anywhere.

Start with the Basics

To begin your loan application, you will need to provide a few key details about your current loan, your vehicle financing, and your overall financial profile. This information helps lenders assess your situation accurately and determine which loan options may be available to you.

Most applications require:

- a valid driver’s license

- vehicle registration

- proof of insurance

- current loan details, including your interest rate and payment terms

What Happens After You Apply

Once your information is submitted, a SafeLend Canada Refinance Specialist will review your application and guide you through the next step. In many cases, this includes a short follow-up to confirm your vehicle information, payment history, and any recent changes that may impact your financial stability.

Lenders are not relying on your credit score alone at this stage. They may also review your credit report, payment consistency, income stability, and existing financial obligations to build a complete picture of your financial position.

Moving Toward Your Options

The goal of this step is to clearly understand your situation so you can be matched with realistic and competitive auto loan refinance options. This is where the process begins to shift from applying to identifying opportunities that can improve your monthly car payments, support your cash flow, and strengthen your financial flexibility.

Most refinance applications can be completed in under 15 minutes, making it a quick and accessible way to explore your options without a major time commitment.

Step 3: Get Matched with the Right Lender for Your Situation

After your refinance application has been reviewed, the next step is being matched with a lender that fits your specific financial profile. Rather than sending your information to multiple lenders at once, SafeLend Canada takes a more focused approach by connecting you with a lender that aligns with your qualifications and financial goals.

A Smarter Way to Compare Loan Options

This part of the auto loan refinancing process is designed to simplify your experience and support better financial decisions. Instead of sorting through multiple offers on your own, your SafeLend Refinance Specialist works behind the scenes to identify a refinancing solution that offers competitive terms based on your situation.

Lenders consider a combination of factors when reviewing your profile, including your credit history, credit scores, income stability, existing financial obligations, and current vehicle financing. This broader approach helps ensure that your loan options are tailored to your full financial picture, not just a single number.

What This Step Can Help You Improve

Depending on your situation, an auto loan refinance may help you:

- lower your interest rate and reduce interest costs

- reduce your monthly car payments to improve cash flow

- adjust your loan term to better match your financial goals

- strengthen your overall loan structure and financial flexibility

Support for More Complex Situations

For some borrowers, this step creates a path forward even when challenges are present. Whether you are dealing with higher interest rates, negative equity, or a lower credit rating, SafeLend Canada works with a network of lending partners that can consider a wider range of financial factors.

This flexibility helps create more realistic and accessible loan options for borrowers who may not fit traditional lending criteria.

From Application to Clarity

At this stage, your focus shifts from applying to understanding your options. Your specialist will walk you through each offer so you can evaluate how it impacts your monthly payments, total interest, and long-term financial health.

The goal is not just approval, it is finding a refinancing solution that supports your financial stability and aligns with your goals moving forward.

Step 4: Review and Sign Your Refinancing Documents

Once you have reviewed your refinancing options and are ready to move forward, the next step is finalizing your new loan. At this stage, your SafeLend Canada Refinance Specialist will walk you through the details so you clearly understand your new interest rate, payment structure, and loan duration. This ensures you are making a confident and informed financial decision based on your current situation.

Review Your New Loan Carefully

Before signing, take a moment to compare your updated loan with your previous vehicle financing. Focus on how the new terms affect your monthly car payments, total interest, and overall financial health.

This quick review helps confirm that your refinancing decision supports your financial stability and long-term goals.

Sign Your Documents Digitally

When everything looks right, your documents will be sent electronically for review and signature. The entire process is completed online, making it fast, secure, and convenient without the need to visit a branch or handle paperwork in person.

Final Details to Confirm

To complete this step, you may be asked to upload or confirm a few final items:

- valid identification

- vehicle registration

- proof of insurance

- loan payout details from your current lender

What Happens After You Sign

Once your documents are signed and verified, your new lender will pay off your existing loan, completing the transition from your current vehicle financing into your updated agreement.

At this point, your auto loan refinance is nearly complete. Your new loan terms will soon take effect, allowing you to move forward with improved financial flexibility and a structure that better fits your needs.

Step 5: Transition to Your New Loan and Start Saving

Once your auto loan refinance is finalized, your new lender will pay off your existing loan and your updated loan terms will take effect. From this point forward, you will begin making payments based on your new agreement, completing the transition from your previous vehicle financing into a structure that better fits your current needs.

What This Means for You

For many borrowers, this is where the real impact of refinancing begins. Depending on your situation, your new loan may provide:

- lower monthly payments

- reduced interest costs over time

- improved cash flow within your monthly budget

- more flexibility in how your loan is structured

A More Manageable Financial Path

Refinancing is not just about replacing one loan with another. It is about creating a setup that works better for your day-to-day life. With the right structure in place, your payments can feel more predictable and easier to manage alongside your other financial obligations.

Over time, staying consistent with your payments can also help strengthen your credit history and credit rating. A loan that fits your income and budget more comfortably reduces financial stress and supports better long-term financial habits.

Looking Ahead

With your new loan in place, you now have a clearer path forward. Whether your goal is interest savings, improved cash flow, or better alignment with your financial priorities, refinancing can help you move in the right direction.

You have now completed the process of how to refinance a car loan in Canada and can begin benefiting from your updated loan terms with greater confidence.

Can You Refinance Your Car Loan More Than Once in Canada?

Yes, you can refinance your car loan more than once in Canada, as long as you continue to meet lender requirements and there is a clear financial benefit to doing so.

Refinancing is not limited to a single opportunity. It can be used strategically over time as your financial situation changes. For example, some borrowers choose to refinance again if their credit score improves, interest rates decrease, or their income becomes more stable. In these cases, a second refinance may help secure better loan terms, such as a lower interest rate or more manageable payments.

When Refinancing Again May Make Sense

You may consider refinancing more than once if:

- your credit score has improved

- interest rates have decreased

- your income or financial situation has changed

- better loan options have become available

What to Consider Before Refinancing Again

Refinancing multiple times should always be approached with a long-term view. Each time you refinance, you are replacing your existing loan with a new one, which may reset your loan term. While this can reduce your monthly payment, it may also increase the total interest paid over time if the term is extended.

Lenders will reassess your situation with each application, including your loan balance, vehicle value, payment history, and overall finances. If your vehicle has depreciated significantly or your loan is close to being paid off, refinancing again may offer limited benefit.

Key Takeaway

The key is to evaluate whether refinancing again improves your financial position, not just whether it is available. When used strategically, refinancing more than once can be a useful tool to adapt your auto loan as your circumstances evolve.

Does Refinancing a Car Loan Affect Your Credit Score?

Yes, refinancing a car loan can affect your credit score, but the impact is usually small and temporary. In many cases, it can actually improve your credit over time if managed properly.

What Happens to Your Credit When You Apply

When you apply for an auto loan refinance, a credit check may be performed. Many lenders begin with a soft inquiry during prequalification, which does not impact your credit score.

If you move forward with a full loan application, a hard inquiry may be required. This can cause a slight, short-term dip in your score, but the effect is typically minimal.

How Refinancing Can Impact Your Credit Over Time

Refinancing replaces your existing loan with a new one, which can slightly affect your credit history by changing the average age of your accounts.

However, the long-term impact often depends on how you manage your new loan. If your refinanced loan offers more manageable payments and you stay consistent with on-time payments, this can strengthen your payment history, which is one of the most important factors in your credit profile.

Why Affordability Matters Most

For many borrowers, the biggest benefit of refinancing is improved affordability. A loan that better fits your budget can reduce financial stress and lower the risk of missed payments.

Missed or late payments have a much greater impact on your credit score than a single inquiry, which is why improving your payment structure can be more important than avoiding a small, temporary dip.

Key Takeaway

Refinancing is not something to avoid because of credit concerns. When used strategically, it can help improve both your loan terms and your credit health over time.

Can You Refinance with Negative Equity or Bad Credit?

Yes, it is possible to refinance your car loan in Canada even if you have negative equity or bad credit, but your refinancing options will depend on your overall financial profile.

Understanding Negative Equity

Negative equity means you owe more on your loan than your vehicle is currently worth. While this can make auto refinancing more complex, it does not automatically disqualify you.

Lenders may still consider your application if your broader financial profile is strong. This includes factors such as your payment history, income stability, and accurate vehicle information, all of which help provide a clearer picture of your situation.

Refinancing with Credit Challenges

Having credit challenges does not mean refinancing is out of reach. Many lenders look beyond your credit score and assess a wider range of factors, including your employment stability, income, and consistency of past payments.

In some cases, auto refinancing can help you move into a loan structure that is easier to manage and better aligned with your current financial situation.

What to Expect

It is important to set realistic expectations. Refinancing with negative equity or credit challenges may not always result in a significantly lower interest rate.

However, it can still provide value by:

- improving your payment structure

- making monthly payments more manageable

- supporting better long-term debt management

- creating a path toward rebuilding your credit over time

Key Takeaway

The key is to explore your refinancing options with a clear understanding of your goals. Even if your situation is not ideal, auto refinancing may still offer a practical way to regain control of your loan and move toward a more stable financial position.

Working with platforms like SafeLend Canada can help simplify this process by connecting you with lenders who understand a range of financial situations and can offer solutions tailored to your needs.

Final Thoughts: Is Refinancing Your Car Loan the Right Next Step?

Refinancing your car loan can be a valuable financial tool, but the right decision depends on your individual situation. Whether you want to lower your monthly payments, reduce interest costs, or better align your loan with your budget, the key is understanding how each option affects your finances over time.

Throughout this guide, we’ve covered how auto refinancing works and answered key questions around credit impact, eligibility, refinancing options, and long-term outcomes. Reviewing your credit report, financial obligations, and key details like your vehicle information and loan payout can help you make more confident decisions when applying.

If refinancing your loan improves your financial position, increases cash flow, or supports greater financial flexibility, it may be the right next step. The goal is not just to replace your existing loan, but to create a structure that supports stronger debt management and long-term financial stability. In some cases, auto refinancing may also help you move toward building positive equity in your vehicle over time and getting on the "Path to Prime."

Exploring your options with SafeLend Canada can help you understand what is available, especially if you are dealing with credit challenges or need more flexible solutions. With a streamlined application process application process and access to multiple lending partners, you can move forward with confidence when the timing is right.

Frequently Asked Questions

Can you refinance your car loan in Canada?

Yes, most Canadians with existing vehicle loans can refinance, provided they meet basic lender requirements such as income stability, vehicle eligibility, and overall financial profile.

How soon can you refinance a car loan?

You can refinance at any time, but many lenders prefer to see a few months of payment history before approving a refinance application, especially for newer vehicle loans.

Does refinancing a car loan affect your credit score?

Refinancing may cause a small, temporary impact due to a credit inquiry, but consistent on-time payments can help improve your credit history and credit rating over time as part of broader credit solutions.

Can you refinance your loan more than once?

Yes, refinancing more than once is possible if it continues to provide a financial benefit, such as better loan options, lower interest rates, or improved payment terms through a new agreement.

Can you refinance with bad credit?

Yes, many lenders offer credit solutions and consider factors beyond your credit score, including income, payment history, and overall financial stability.

Can you refinance a car with negative equity?

It is possible, although your loan options may be more limited. Some lenders will still work with borrowers based on their full financial profile, even if the balance exceeds the current vehicle value.

What do you need for a refinance application?

You typically need identification, vehicle details, proof of insurance, and information about your current loan, including your balance, interest rate, and in some cases a loan payout statement.

How long does the application process take?

Most refinance applications can be completed in under 15 minutes, with approvals often processed quickly and supported by secure online access to your application and documents.

Will refinancing lower my monthly car payments?

It can, depending on your new interest rate and loan term, but it is important to also consider the total interest paid over the life of the loan and whether the structure supports your long-term goals.

Where can you apply for auto loan refinancing?

You can apply online through platforms like SafeLend Canada, which connect you with lenders based on your financial profile and refinancing needs, without requiring a trade-in process or purchasing a new vehicle.

Are there prepayment penalties when refinancing a car loan?

Most lenders do not charge prepayment penalties, but it is important to review your current loan agreement to confirm whether any fees apply before completing a refinance.

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.