Last Updated: February 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: November 2023

By: Danielle Burton

Category: Auto Refinancing

How to get out of a car loan in Canada often becomes urgent when your monthly loan payment starts creating real financial burdens. If your interest rate is high, your payoff amount barely seems to shrink, or you feel underwater on your car loan because the market value no longer matches what you owe, you are not alone. Many Canadians find themselves stuck in auto financing debt that strains their budget and risks pulling them deeper into a debt cycle.

The good news is that you have options. In many cases, auto loan refinancing lets you replace your current loan with a new one that may lower your interest rate, reduce your monthly payment, or adjust your term without giving up your vehicle. Depending on your car’s value, credit score, and remaining payoff amount, refinancing can provide debt relief and help you avoid missed payments or further financial trouble.

In this guide, you’ll learn how the refinancing process works in Canada, how lenders assess approval based on your credit score, income, and vehicle value, and what fees to review before signing a new loan. You’ll also consider options like selling your vehicle, negotiating with your lender, or exploring other solutions if refinancing isn’t right for you.

QUICK ANSWER:

You can get out of a car loan in Canada by refinancing to lower your rate or payment, selling or trading your vehicle, or asking your lender for hardship support. The best option depends on your payoff amount, credit score report, loan contract terms, and whether you are underwater on your car loan. Comparing the full refinancing process and total cost of borrowing is essential before making a decision.

In This Guide (Your Road Map to Auto Loan Relief)

- 1. What Are the Benefits of Auto Loan Refinancing in Canada?

- 2. How Does Your Credit Score Affect Auto Loan Refinancing Approval?

- 3. What Auto Loan Refinancing Options Are Available in Canada?

- 4. What Fees and Hidden Costs Should You Watch for When Refinancing a Car Loan?

- 5. When Is the Best Time to Refinance a Car Loan in Canada?

- 6. How Do You Refinance a Car Loan in Canada Step by Step?

- 7. What Are Your Options if You Want Out of a Car Loan in Canada?

- 8. Final Thoughts: Is Auto Loan Refinancing Worth It?

- 9. Frequently Asked Questions About Auto Loan Refinancing in Canada

What Are the Benefits of Auto Loan Refinancing in Canada?

Before starting the refinancing process, review your payout amount, confirm your vehicle’s current market value, and ensure the proposed financing agreement truly lowers your total cost instead of simply extending your debt. Auto loan refinancing replaces your existing loan contract with a new one, ideally offering better terms and real debt relief. Based on your credit profile, remaining balance, and whether you are facing financial burdens or an upside-down car loan, it may:

- reduce your interest rate

- lower your monthly car payment

- adjust your repayment term

- improve your overall financial flexibility

Below are the most common benefits of auto loan refinancing in Canada.

Lower Interest Rates: A Gateway to Savings

One of the main reasons Canadians choose to refinance is to secure a lower interest rate . If your original loan was approved when rates were higher or when your credit score was weaker, you may now qualify for better terms. Even a modest rate reduction can have a meaningful impact. For example, lowering your rate from 7% to 4% can reduce the total interest paid over the life of the loan and allow more of each monthly payment to go toward the principal.

Reduced Monthly Payments: Lightening the Load

Refinancing can reduce your monthly payment, which may provide meaningful relief if your current vehicle loan is straining your budget. In some cases, extending your loan term lowers the payment, for example, moving from a 48-month term to 60 months could reduce a $500 payment closer to $400. While total interest may increase, the added flexibility can help prevent missed payments and protect your credit.

More Flexibility and Control Over Your Loan Term

Refinancing is not only about securing a lower interest rate, it can also give you greater control over how your loan fits your financial situation. Depending on your goals, you may shorten the term to pay off the balance faster or extend it to reduce your monthly payment. This added flexibility can help manage unexpected expenses, stabilize cash flow, and lower the risk of missed payments.

Auto loan refinancing in Canada can help lower borrowing costs and improve financial stability, but approval is not guaranteed. Before moving forward with refinancing, it’s important to review your current loan payout amount, assess your vehicle’s market value, and carefully compare the proposed new terms. Make sure the refinance truly lowers your total cost, reduces your monthly payment, or shortens your loan term, rather than just extending your debt.

How Does Your Credit Score Affect Auto Loan Refinancing Approval?

When it comes to auto loan refinancing in Canada, your credit score is one of the primary factors lenders use to determine whether you qualify and what interest rate you will be offered. A stronger credit profile can improve approval odds and lead to lower borrowing costs, while a lower score may limit available options or result in higher rates and stricter terms.

That said, your credit score is not the only factor lenders consider during the refinancing process. Loan approval for auto loan refinancing also depends on your income stability, total debt levels, debt-to-income ratio, and how your vehicle’s market value compares to your remaining balance. Lenders review these factors together to assess overall risk, determine appropriate interest rates, and decide what loan contract terms you may qualify for.

Why Credit Score Matters for Auto Loan Refinancing

Your credit score reflects how consistently you’ve managed credit over time and plays a major role in the refinancing process. It is calculated using factors such as your payment history, credit utilization, total debt levels, and the length of your credit history. Lenders review this information to assess risk and determine your likelihood of loan approval and interest rate eligibility.

Here’s how your credit score can affect refinancing:

- Approval chances: A higher score improves your ability to qualify, while a lower score may reduce available lender options.

- Interest rate offered: Better credit usually means lower interest rates, which can reduce your monthly payment and total borrowing cost.

- Loan terms: Strong credit may qualify you for shorter terms, better repayment flexibility, or fewer lender fees.

If you’re currently dealing with a high interest car loan , improving your credit score may help you access more affordable refinancing options.

What Lenders Look at Besides Your Credit Score

Even if your score is not perfect, you may still qualify depending on your overall financial picture.

Many Canadian lenders also evaluate:

- Income and job stability

- Debt-to-income ratio (DTI)

- Payment history on your current loan

- Vehicle value vs loan balance (loan-to-value ratio)

- Length of time you’ve had the loan

- Down payment or equity position

This is why refinancing can still be possible for some borrowers with non-prime credit, especially if they have steady income and consistent payments.

How to Improve Your Credit Score Before Refinancing

If you want to improve your approval odds or qualify for a lower rate, here are some of the most effective steps:

- Check your credit report for errors and dispute any incorrect information

- Make all payments on time, including credit cards and loans

- Pay down revolving debt, especially high credit card balances

- Avoid applying for new credit before refinancing, too many inquiries can temporarily lower your score

- Keep credit utilization low, ideally under 30% of your available limit

- Build positive history by keeping accounts active and in good standing

If your credit situation feels overwhelming, a non-profit credit counselling service can also help you create a plan to reduce debt and rebuild your score over time.

What Auto Loan Refinancing Options Are Available in Canada?

When refinancing a car loan in Canada, you generally have three main options: using an online lender, refinancing through a dealership, or applying directly with a bank. Each option has different approval rules, timelines, paperwork requirements, and levels of flexibility. Comparing them carefully helps ensure the choice you make aligns with your credit profile, budget, and long-term financial goals.

Here is a breakdown of the most common refinancing routes Canadians consider.

SafeLend Canada: Online Refinancing with Multiple Lender Options

SafeLend Canada offers an online refinancing process that connects borrowers with multiple lenders through a single application, helping streamline the path to loan approval. The entire process is SafeLend Canada offers an online refinancing process that connects borrowers with multiple lenders through a single application, helping streamline the path to loan approval. The entire process is completed digitally, making it more convenient and accessible for many applicants facing financial burdens or monthly loan payment pressure. In many cases, decisions are faster than traditional bank or dealership financing, depending on eligibility and documentation.

Best for: Canadians who want a fast online process, flexible lender matching, and want to keep their vehicle.

Key benefits may include:

- access to lenders across a wide range of credit profiles

- competitive refinancing offers (subject to approval)

- options to lower your monthly payment or adjust your loan term

- a streamlined application process with fewer steps than a bank branch

- no trade in necessary

This option may be a good fit if you're trying to reduce your payment, refinance a high-interest loan, or explore refinancing without visiting a dealership.

Dealership Refinancing: Convenient, Especially When Trading In

Refinancing through a dealership can be appealing if you are trading in your vehicle, upgrading to a newer model, or rolling your existing loan into a new purchase. Dealerships often coordinate financing through partner lenders and handle much of the paperwork for you. This can simplify the process, save time, and make the overall experience feel more convenient for many borrowers.

Best for: Drivers who are trading in their vehicle or switching to a more affordable car.

Things to consider:

- promotional offers may be available for certain vehicles

- fees, add-ons, or warranties may be rolled into the new loan

- refinancing options may be limited to the dealership’s lender partners

- borrowers with non-prime credit may have fewer choices

Dealership refinancing can work well, but it is important to review the loan details carefully, especially the final interest rate, total loan amount, and any extras added to the agreement.

Traditional Banks: Reliable, but Often More Restrictive

Some Canadians choose to refinance through a traditional bank because they value the stability, structure, and familiarity of working with a major financial institution. Banks may offer competitive interest rates and established lending processes, but their loan approval standards are typically stricter. They often require higher credit scores, stronger income verification, and more detailed documentation before approving a new financing agreement or restructuring an existing loan contract.

Best for: Borrowers with strong credit and stable income who want a traditional lending experience.

Some limitations to consider:

- stricter credit score and approval standards

- longer processing times and more documentation

- fewer flexible options for borrowers rebuilding credit

- less willingness to refinance higher-risk vehicle loans

If you have excellent credit, a bank may offer strong rates, but if your credit is recovering, other refinancing routes may provide more flexibility.

Choosing the right refinancing option depends on your credit profile, your vehicle’s market value, and your broader financial goals. The best approach is to compare multiple offers carefully, review the full refinancing process, and understand the total cost outlined in each financing agreement. Evaluate interest rates, fees, and repayment terms closely. Prioritize long-term affordability, flexibility, and meaningful savings instead of focusing only on quick loan approval decisions.

What Fees and Hidden Costs Should You Watch for When Refinancing a Car Loan?

Auto loan refinancing can lower your interest rate and monthly loan payment, helping reduce financial burdens, but hidden fees can quickly reduce your overall savings if you are not careful. Before signing a new financing agreement or loan contract, review the full refinancing process, confirm all costs, and understand how fees affect your total borrowing cost and long-term debt relief goals.

Below are the key fees to watch for.

1. Prepayment Penalties

Some auto loan contracts include early payout fees (also called prepayment penalties). These are designed to discourage borrowers from paying off the loan early.

Why it matters: If your current loan has a penalty, it may reduce or eliminate the savings refinancing was supposed to create. Always request your payout statement and confirm whether any penalty applies.

2. Loan Origination Fees

Some lenders charge an origination fee to set up the new loan and process the paperwork.

Why it matters: Origination fees can increase the total amount you borrow, which may reduce the benefit of a lower interest rate. Make sure the total cost of the loan still makes sense, not just the monthly payment.

3. Application Fees

Some lenders charge a fee just to submit or process your refinancing application.

Why it matters: Small application fees can add up, especially if you apply to multiple lenders to compare offers. Ask upfront whether the application is free.

4. Title Transfer and Registration Fees

Depending on your province, refinancing may require updates to your vehicle registration or lien information, which can involve administrative costs.

Why it matters: These fees are often overlooked, but they should be included when calculating the true cost of refinancing. Ask whether the lender covers these costs or if you are responsible.

5. Late Payment Fees

Late payment charges are not specific to refinancing, but they can become a problem if your payment date changes or you miss the first few payments under your new loan.

Why it matters: Late payments can damage your credit score and increase your overall loan cost. In serious cases, missed payments can lead to repossession.

6. Document and Credit Report Fees

Some lenders add small administrative charges such as document preparation fees, lien registration fees, or credit report processing costs.

Why it matters: These fees may seem minor, but they can still reduce your overall savings. Always review your loan breakdown carefully and ask about any unclear line items.

How to Avoid Hidden Fees When Refinancing

The best way to protect yourself is to compare offers and ask the right questions before signing.

Before you refinance, confirm:

- Is there a prepayment penalty on my current loan?

- Are there origination or administration fees?

- Is the interest rate fixed or variable?

- What is the total cost of borrowing, not just the monthly payment?

- Are registration or title transfer fees included?

- Can I make extra payments without penalty?

Choosing a lender or refinancing provider that clearly explains all fees upfront can help you avoid surprises and make a more confident decision.

When Is the Best Time to Refinance a Car Loan in Canada?

1. Interest Rates Have Dropped

Auto loan rates fluctuate over time, and if current rates are noticeably lower than the rate on your existing loan, refinancing may help reduce your monthly payment or the total interest you pay. Before moving forward, compare your current interest rate with new offers carefully. Even a 1 to 2 percent reduction can result in meaningful savings, particularly if you still have several years remaining on your loan term.

2. Your Credit Score Has Improved

If your credit score has improved since you first financed your vehicle, you may now qualify for better loan terms and lower interest rates through auto loan refinancing. This often applies to borrowers who began with non-prime credit and have since strengthened their payment history, reduced outstanding debt, and demonstrated greater financial stability, improving their chances of loan approval and better financing agreement terms.

A higher credit score can lead to:

- lower interest rates

- better loan terms

- more lender options

Checking your credit before applying can help you understand whether refinancing will produce real savings.

3. Your Income or Financial Stability Has Increased

A stronger income or more stable employment can improve your approval odds and expand your refinancing options.

If your financial position has improved, you may qualify for a shorter loan term or better rate, helping you pay off your vehicle faster and reduce total interest costs.

4. You Are Midway Through Your Loan Term

Refinancing can make sense once you have paid down a portion of your principal balance, as your loan-to-value ratio may improve, especially if your vehicle has retained its market value. Review your loan statement to see how much principal remains. If you still carry a significant balance and better rates are available, refinancing could help you restructure the remaining term more efficiently.

5. Your Financial Goals Have Changed

Your financial priorities may shift over time. You may want to:

- reduce your monthly expenses

- free up cash flow before a mortgage renewal

- lower your debt-to-income ratio

- pay off your vehicle sooner

Refinancing can help align your car loan with your current goals rather than the ones you had when you first signed the agreement.

You Should Consider Refinancing If:

- your current rate is much higher than available rates

- your credit score has improved

- your monthly payment feels too high

- you want to lower your debt-to-income ratio

- you need more flexibility in your loan structure

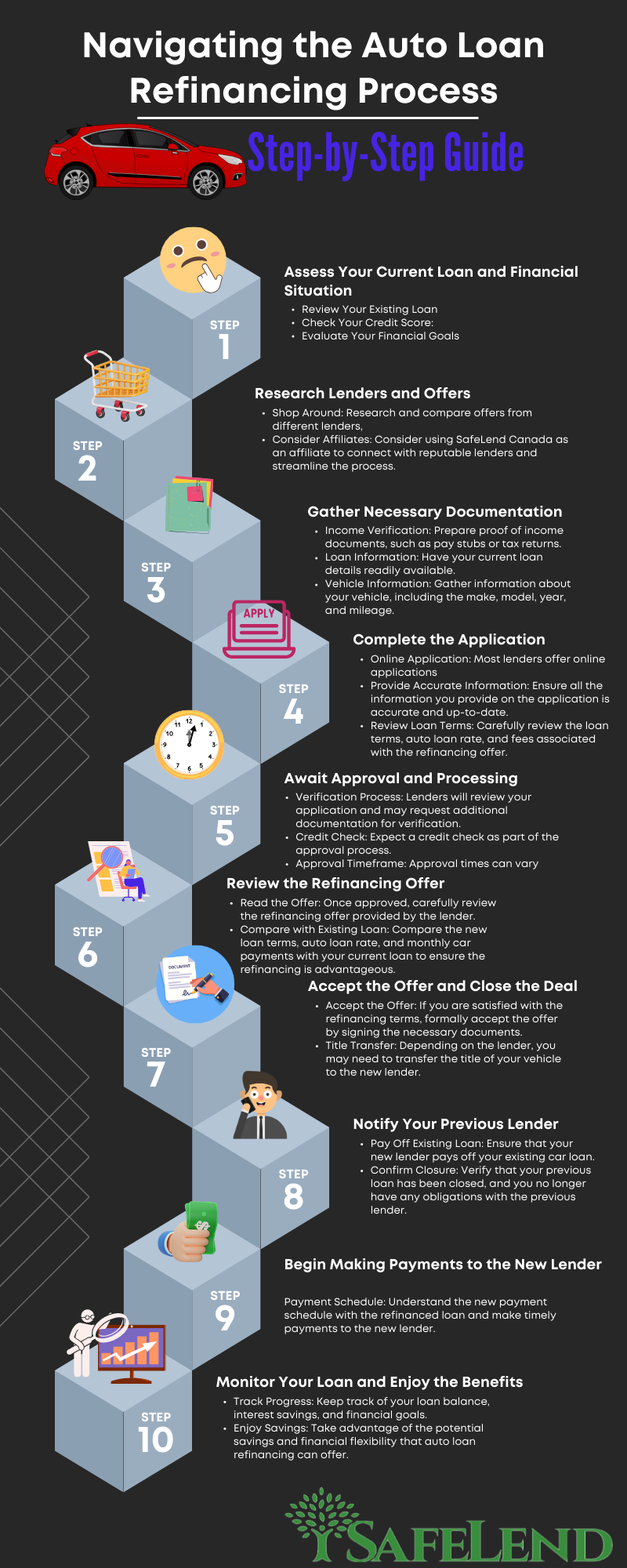

How Do You Refinance a Car Loan in Canada Step by Step?

Refinancing a car loan in Canada is usually straightforward when you understand what information lenders require and how to properly compare offers. The goal is to replace your current auto loan with a new one that provides better terms, such as a lower interest rate, a reduced monthly payment, or a loan term that better fits your budget and long-term financial plans.

Here is a step by step process you can follow.

If your goal is to improve your credit, consistent on time payments matter more than anything else.

QUICK ANSWER: Refinancing is only a win if the new loan improves your total cost, your monthly affordability, or your ability to stay on track. Always review the full cost of borrowing, not just the headline rate.

What Are Your Options if You Want Out of a Car Loan in Canada?

If refinancing is not the right fit, or if you want to review every available solution before making a decision, there are several ways to reduce or eliminate your car loan. The best option depends on your remaining loan balance, your vehicle’s value, your income, and whether your situation is temporary or long term.

| Option | Description | Key Benefits | Considerations |

|---|---|---|---|

| Auto Loan Refinancing | Apply for a new loan to replace your existing car loan with better terms, potentially lowering payments and interest costs. | Competitive auto loan rate, Same-day decisions, Simple application process through SafeLend Canada | Eligibility requirements, Lower Payments, Keep your vehicle and no hidden costs |

| Loan Modification with Current Lender | Negotiate with your current lender to modify loan terms, such as lowering interest rates or extending the loan for lower payments. | Familiarity with lender, Customer service support | Lender's willingness and ability to modify terms |

| Sell or Trade-In Your Vehicle | If payments are unmanageable, consider selling or trading your car. Use the proceeds to pay off the loan or secure a more affordable vehicle. | Financial relief from car payments, Equity position | Vehicle's value and potential negative equity |

| Seek a Shorter-Term Loan | Opt for a shorter-term auto loan to pay off the loan faster and reduce overall interest costs. | Faster loan payoff, Reduced interest expenses | Higher monthly payments, Assess monthly income |

| Explore Loan Assistance Programs | Some lenders offer programs for temporary relief through deferred payments or modified loan terms. | Temporary financial relief, Lender assistance | Availability and eligibility criteria |

| Budget and Financial Counseling | Seek guidance from a financial counselor for holistic financial improvement, budgeting, expense management, and goal-setting. | Comprehensive financial planning, Expert advice | Requires commitment and discipline |

| Consider Selling to a Private Buyer | Sell to a private buyer who pays off the auto loan, avoiding negative equity and potentially fetching a higher sale price. | Avoid negative equity, Potential higher sale price | Finding a buyer willing to pay off the loan |

| Evaluate Your Financial Goals | Define your financial objectives, whether it's reducing expenses, lowering interest rates, or aligning with financial goals. | Tailored solution to meet goals, Informed decisions | A clear understanding of your goals is essential. |

How to Decide Which Option Is Right for You

Before making a decision, take a step back and evaluate your situation carefully.

Ask yourself:

- Do I want to keep this vehicle long term?

- Is my main issue the interest rate or the monthly payment?

- Do I have equity, or do I owe more than the vehicle is worth?

- Is my financial challenge temporary or ongoing?

- Will this option lower my total cost, or just stretch out the debt?

If you want to keep your vehicle and improve your interest rate or payment structure, refinancing through a bank or an online platform that connects you with multiple lenders may be worth considering. However, if the vehicle no longer fits your budget, selling, trading down, or negotiating new terms with your current lender could offer a cleaner financial reset. The best solution is not always the one with the lowest monthly payment, but the one that strengthens your overall financial position and supports long-term stability.

Final Thoughts: Is Auto Loan Refinancing Worth It?

Auto loan refinancing can be worth it if it meaningfully lowers your monthly loan payment, reduces your interest rate, or improves the structure of your financing agreement. The goal is not just loan approval, but real financial improvement, whether through lower payments, reduced total borrowing costs, faster payoff of your remaining balance, or a personalized plan that eases ongoing financial burdens and supports long-term financial stability.

For many Canadians, refinancing makes sense when:

- their current interest rate is too high

- their credit score report has improved since the original car purchase

- their monthly loan payment is creating ongoing financial burdens

- they want to lower their debt-to-income ratio

- their vehicle’s market value supports better refinancing loans

- they are underwater on their car loan and looking for a more manageable path forward

Refinancing is not right for everyone. If fees cancel out the savings, a hard inquiry doesn’t lead to better terms, or extending the loan increases long-term debt, another solution may be better. In some cases, negotiating with your lender, speaking with a credit union, or exploring structured debt relief can help you avoid falling deeper into debt or facing collections.

Before signing any new financing agreement, take time to review the full refinancing process carefully and understand each step involved. Confirm that your VIN and vehicle details are accurate, review the total cost of borrowing, and compare offers from banks, credit unions, or online lenders such as SafeLend Canada. Ensure the new loan meaningfully improves your affordability and long-term financial stability, rather than burying you deeper into debt.

If your current car loan no longer fits your financial reality, taking time to assess your options is a smart step toward reducing financial burdens and regaining control of your future.

Frequently Asked Questions About Auto Loan Refinancing in Canada

1. What is auto loan refinancing, and how does it work?

Auto loan refinancing means replacing your current car loan with a new one, usually from a different lender. The new loan may offer a lower interest rate, a lower monthly payment, or a different term. If approved, the new lender pays off your old loan and you begin making payments under the new agreement.

2. Is auto loan refinancing worth it in Canada?

Refinancing can be worth it if it lowers your interest rate, reduces your monthly payment, or improves your overall loan structure. It is most beneficial when your credit score has improved or when current interest rates are lower than your original loan. Always compare the total cost of borrowing before deciding.

3. Will refinancing hurt my credit score?

Applying for refinancing may trigger a hard credit inquiry, which can temporarily lower your score by a few points. However, making consistent on time payments on your new loan can improve your credit over time. The long term impact is often positive if the loan is managed properly.

4. Can I refinance a car loan with bad credit?

Yes, refinancing with bad or non-prime credit is possible, but options may be more limited and interest rates may be higher. Some lenders consider income stability and payment history in addition to credit score. Improving your credit before applying can increase your chances of securing better terms.

5. When is the best time to refinance a car loan?

While it may be more challenging to refinance with bad credit, it's not impossible. Some lenders specialize in working with borrowers with less-than-perfect credit. However, you may encounter higher interest rates and less favorable terms. Improving your credit score before refinancing can help you secure better rates.

6. Can I refinance if my car has high mileage?

It depends on the lender and the vehicle’s age. Some lenders have mileage or age limits, while others are more flexible. The vehicle’s value compared to your loan balance also plays a role in approval.

7. Can I refinance if I owe more than my car is worth?

Refinancing with negative equity can be more difficult, but it may still be possible depending on your credit profile and income. Some lenders have limits on loan-to-value ratios. If the gap is too large, you may need to cover part of the difference.

8. Are there hidden fees when refinancing a car loan?

There can be fees such as prepayment penalties, origination charges, or lien registration costs. Always review the full loan breakdown and confirm the total cost of borrowing before signing.

9. How much can refinancing save in Canada?

Savings vary depending on your loan balance, interest rate reduction, and remaining term. Even a 1 to 2 percent rate drop can save hundreds or thousands of dollars over the life of the loan. The best way to estimate savings is to compare total interest costs between your current loan and the new offer.

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.