Last Updated: March 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: February 2026

By: Danielle Burton

Category: Negative Equity

Negative equity on a car happens when your auto loan balance is higher than your vehicle's current market value. This negative car equity situation happens when the total amount financed under your auto loan is higher than your vehicle's current market value. It is often called being upside down on a car loan, and it usually happens when long loan terms, high interest, rolled over debt, or fast depreciation prevent your balance from dropping quickly.

Many Canadians enter a car finance agreement focused primarily on securing an affordable monthly vehicle payment. Even if your monthly vehicle payment feels manageable, much of it may go toward interest in the early years, slowing how quickly you build equity. Add-ons financed through car dealers, such as extended warranties or protection packages, increase the total price of the vehicle and can create negative equity from the start. A low cash down payment or no down payment at all further raises the loan to value ratio, increasing exposure to car depreciation.

Negative equity on a car matters because it limits financial flexibility. It can complicate the trade-in process, restrict refinance options, and increase total borrowing costs over the life of the finance agreement. If your credit report improves or interest rates change, refinancing may help, but lenders still evaluate your current negative equity position and overall loan structure before approving new vehicle loans. Without strategic planning, the gap between your loan payoff amount and your car value can widen over time.

In this guide, you will learn:

- What negative equity on a car really means

- How car depreciation and long-term loans contribute to negative car equity

- How to calculate your equity position using your payoff amount and current car value

- The warning signs of a negative equity vehicle situation

- Smart strategies to reduce risk in future car finance decisions

If you are unsure where your current auto loan contract stands, now is the time to carefully review your loan payoff balance, total interest payments to date, and your vehicle's realistic market value. Comparing these numbers helps you understand your true equity position. The earlier you identify a negative equity situation, the more control you have over your car finance strategy and long term financial stability.

In This Guide: Understanding and Fixing Negative Equity

- 1. What Is Negative Equity on a Car and Why Does It Matter?

- 2. How Does Negative Equity on a Car Happen?

- 3. What Are the Warning Signs of Negative Equity on a Car?

- 4. How Does Vehicle Depreciation Affect Negative Equity on a Car?

- 5. Can Refinancing Fix Negative Equity on a Car?

- 6. Does Trading In a Car With Negative Equity Make Things Worse?

- 7. How Can You Avoid Negative Equity on a Car in the Future?

- 8. Final Thoughts on Negative Equity on a Car

- 9. Frequently Asked Questions

What Is Negative Equity on a Car and Why Does It Matter?

Negative equity on a car occurs when your auto loan balance is higher than your vehicle's current market value. In practical terms, you owe more under your car finance agreement than the car value would generate if sold today. This negative car equity position, often called being upside down on a car loan, typically develops when the total price of the vehicle financed exceeds its depreciated resale value.

For example, if your loan payoff amount is $25,000 but your vehicle's current market value is only $20,000, you are carrying $5,000 in negative equity. That $5,000 difference represents the shortfall between your remaining balance under the auto loan contract and the price the vehicle could realistically sell for in today's resale market conditions.

Why Negative Equity on a Car Matters

Negative equity affects more than just numbers on a statement. It can impact your flexibility, borrowing costs, and future financing decisions.

Here's how:

- It complicates the trade-in process. If you sell or trade in your vehicle, you must either pay the shortfall out of pocket or consider rolling over debt into a new finance agreement.

- It increases total loan costs. Rolling negative equity into future vehicle loans raises your starting principal and increases long term interest payments.

- It may limit refinance options. Lenders assess your loan to value ratio, credit report, and overall car finance structure before approving a refinance. A higher loan to value ratio increases perceived risk.

- It extends exposure to depreciation. Long-term loans combined with elevated interest rates can allow car depreciation and shifting depreciation rates to outpace principal reduction.

Over time, this negative equity position can widen if the monthly vehicle payment structure does not aggressively reduce the balance.

The Key Risk to Understand

When principal reduction happens more slowly than car depreciation, the gap between your loan balance and your vehicle's market value continues to widen over time. As this imbalance grows, a standard car finance agreement can gradually shift into a negative equity vehicle situation. This means you owe more under your auto loan contract than the car is realistically worth in today's resale market.

Understanding your equity position early helps you decide whether refinancing, adjusting your loan, or paying down the balance faster is the right move.

How Does Negative Equity on a Car Happen?

Negative equity on a car happens when your auto loan balance declines more slowly than your vehicle's market value. Because vehicles depreciate quickly, especially during the first few years of ownership, the gap between what you owe and what the car is worth can grow rapidly. Financing decisions such as long term loans, high interest rates, or minimal down payments can widen that gap even further.

In simple terms, when depreciation outpaces principal reduction, an upside down car loan begins to form.

Here are the most common causes:

1. Rapid Vehicle Depreciation

Most vehicles lose a significant portion of their value within the first few years. The moment you drive off the lot, resale value drops. If your loan payoff amount does not decline at the same pace, negative equity on a car can develop quickly, particularly during the first 24 to 36 months.

2. Long Loan Terms

Extended loan terms, such as 72, 84, or 96 months, reduce your monthly payment but slow how quickly you build equity. In the early years of a long term auto loan, a large portion of each payment goes toward interest rather than principal. This keeps your loan balance high while depreciation continues.

The longer the term, the longer you may remain exposed to a high loan to value ratio.

3. Low or No Down Payment

A small or zero down payment means you begin the loan with little or no equity cushion. Without upfront equity, even normal depreciation can immediately push your loan into negative territory.

A higher starting loan to value ratio increases the likelihood of becoming upside down early in the loan.

4. High Interest Rates

Higher interest rates increase the portion of each payment that goes toward interest rather than principal. When more money is allocated to interest, your loan balance declines more slowly, extending the period where negative equity on a car can persist.

This is especially relevant for borrowers who financed during higher rate environments.

5. Rolling Over Previous Debt

If you traded in a vehicle with negative equity and added the remaining balance into your new auto loan, that amount increases your starting principal. This rollover debt immediately inflates your loan balance beyond the vehicle's value.

Repeated rollovers can compound negative equity across multiple vehicle purchases.

6. Financing Add-Ons and Fees

Extended warranties, gap coverage, protection packages, and dealer fees are frequently rolled into your auto loan rather than paid upfront. While some of these add-ons may offer legitimate value, financing them increases your principal balance and raises the total interest paid over the life of the loan. The larger the financed amount, the more likely depreciation will outpace repayment and contribute to negative equity.

Negative equity on a car rarely results from just one decision. It typically develops from a combination of car depreciation, interest rates, long term loans, and the structure of the original auto loan contract. Identifying the root cause of the imbalance is critical. Once you understand what created the gap, you can decide whether refinancing, making extra principal payments, or keeping the vehicle longer is the most practical solution.

What Are the Warning Signs of Negative Equity on a Car?

>

>

Negative equity on a car does not always feel obvious at first. Your monthly payment may seem affordable, but the real issue is the growing gap between your auto loan balance and your vehicle's current market value. Because depreciation happens gradually and loan balances decline slowly in the early years, many drivers do not realize they are upside down until they attempt to refinance or trade in.

Here are the most common warning signs of negative equity on a car:

1. Your Loan Balance Is Higher Than Online Valuations

If you compare your vehicle's estimated resale value using appraisal tools to your loan payoff amount and the payoff is higher, you are likely carrying negative equity. A widening gap between market value and outstanding balance is the clearest indicator.

2. You Owe More Than Your Trade In Offer

If a dealership's trade in offer is lower than what you owe, the difference represents negative equity. This becomes especially apparent during purchase negotiations, when the remaining balance must either be paid out of pocket or rolled into a new loan.

3. Your Loan to Value Ratio Is High

If your loan amount significantly exceeds the vehicle's value, your loan to value ratio may be elevated. Lenders review this ratio when assessing refinance applications. A high ratio can signal limited flexibility and increased financial risk.

4. You Financed Add-Ons or Previous Debt

If extended warranties, service contracts, protection packages, or rollover balances were included in your financing, your original loan amount may have started above the vehicle's value. This increases the likelihood of negative equity from the beginning.

5. You Chose a Long Term Loan With Little Down Payment

Extended terms combined with minimal upfront payment slow principal reduction. If you are early in a 72 to 96 month loan, a large portion of your payment may still be going toward interest rather than principal, increasing the risk that depreciation has already pushed you upside down.

6. Your Vehicle Has Depreciated Faster Than Expected

High mileage, accident history, changing market demand, or economic shifts can reduce resale value more quickly than anticipated. When depreciation outpaces principal reduction, negative equity grows.

How to Confirm If You Have Negative Equity on a Car

To determine your equity position, take these steps:

- Request your current loan payoff amount from your lender.

- Estimate your vehicle's realistic market value using multiple valuation sources.

- Subtract the vehicle value from your payoff balance.

If the result is negative, that number represents your negative equity amount.

Reviewing this calculation regularly allows you to track changes in your loan to value ratio and monitor how your balance compares to your vehicle's market value over time. Catching negative equity early gives you more options, such as refinancing, making extra payments, or keeping the vehicle longer. Clear numbers help you act strategically rather than reacting under pressure.

How Does Vehicle Depreciation Affect Negative Equity on a Car?

Vehicle depreciation is the primary driver of negative equity on a car. Depreciation refers to the rate at which a vehicle's market value declines over time, with the steepest drops typically occurring during the first few years of ownership. As car value decreases quickly in those early years, it can outpace loan repayment and contribute to a negative equity position.

Most vehicles lose a significant portion of their resale value early on. The moment a new car is driven off the lot, its value drops. In many cases, vehicles can lose 15 to 25 percent of their value within the first year alone. This rapid decline can quickly shift your loan to value ratio if your auto loan balance does not decrease at the same pace.

When depreciation outpaces principal reduction, negative equity on a car begins to form.

Why Vehicle Depreciation Outpaces Auto Loan Payoff

Auto loans are typically structured so that early payments go primarily toward interest rather than reducing the principal balance. As a result, your loan balance declines slowly during the first several years of the finance agreement. At the same time, your vehicle's market value may be dropping quickly due to car depreciation, which increases the likelihood of falling into negative equity.

This imbalance increases the risk of becoming upside down on your car loan, particularly when combined with:

- Long loan terms

- Low or no down payments

- Financed add-ons and fees

- Rolled over negative equity from a previous vehicle

- Higher interest rates

When depreciation is aggressive and principal reduction is slow, the equity gap widens and refinancing flexibility may become more limited.

What Causes a Vehicle to Lose Value Faster?

Certain factors can accelerate value loss beyond normal expectations:

- High mileage

- Accident history

- Poor maintenance records

- Shifts in market demand for certain vehicle types

- Fuel price fluctuations or broader economic conditions

These factors can reduce your vehicle's market value faster than anticipated, increasing the likelihood of carrying negative equity on a car when you attempt to trade in or refinance.

Depreciation is unavoidable, but long term negative equity does not have to be. The key is structuring your auto loan carefully from the beginning. By selecting an appropriate loan term, competitive interest rate, and meaningful down payment, you can better align your repayment schedule with how your vehicle's market value is expected to decline over time.

When you understand how depreciation affects your loan balance, you can make smarter decisions about down payments, loan terms, extra payments, or when to refinance.

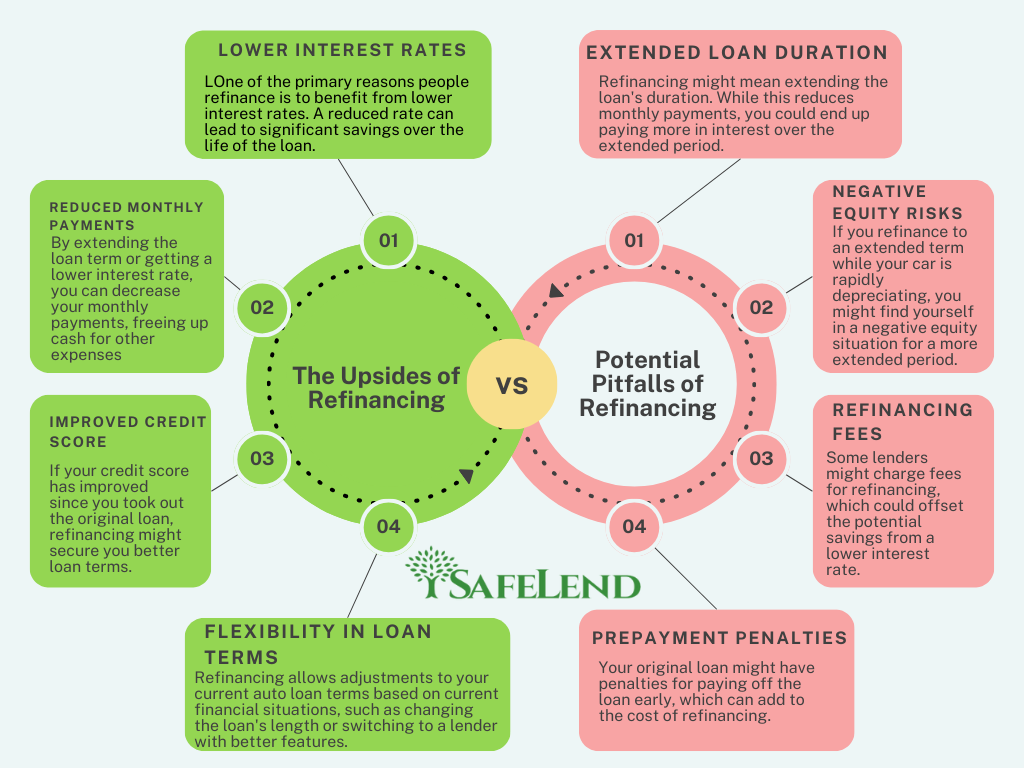

Can Refinancing Fix Negative Equity on a Car?

Refinancing can help manage negative equity on a car, but it does not automatically eliminate the equity gap. Its depends on several factors, including your current auto loan balance, your vehicle's realistic market value, your credit profile, the prevailing interest rate environment, and specific lender guidelines. Reviewing these factors carefully helps you decide whether refinancing truly improves your financial situation.

In simple terms, refinancing replaces your existing auto loan with a new one. When structured strategically, it may:

- Lower your interest rate

- Reduce your monthly payment

- Adjust your loan term

- Improve overall cash flow flexibility

- Accelerate principal reduction under the right conditions

However, if your loan balance significantly exceeds your vehicle's current market value, refinancing options may become more limited. Lenders carefully review your loan to value ratio when evaluating refinance applications, along with your credit profile and repayment history. A high loan to value ratio increases perceived risk from a lending perspective, which can affect approval decisions, interest rate eligibility, or additional required conditions.

When Can Refinancing Help With Negative Equity?

Refinancing negative equity on a car may be beneficial if:

- Your credit score has improved since your original financing

- Interest rates are lower than when you secured your loan

- You need to reduce your monthly payment to stabilize cash flow

- You want to restructure your loan to better align with your budget

- You are trying to prevent rolling debt into a future trade in

Lowering your interest rate allows a greater portion of each monthly vehicle payment to go toward reducing your principal balance rather than covering interest payments. As more of your payment is applied directly to the loan amount, your balance can decline more efficiently. Over time, this can help narrow the negative equity gap and gradually improve your overall loan to value ratio.

When Refinancing May Not Be the Right Move

Refinancing may not fully resolve negative equity if:

- The negative equity amount is substantial

- Extending the loan term significantly increases total interest paid

- The vehicle continues to depreciate rapidly

- The new loan structure delays principal reduction

In some situations, keeping the vehicle longer and making additional principal payments may be the more cost effective strategy for rebuilding equity.

Does Trading In a Car With Negative Equity Make Things Worse?

Trading in a car with negative equity can worsen your position if the remaining balance is rolled into a new auto loan without addressing the equity gap. During the trade in process, the dealership applies the vehicle's market value toward your existing loan payoff. If that amount falls short, the difference is added to your next loan, increasing your starting principal balance and total borrowing costs.

For example:

- You owe $22,000

- Your trade in offer is $18,000

- You have $4,000 in negative equity

That $4,000 is commonly rolled into the financing for your next vehicle, immediately raising your loan to value ratio before you drive away.

Why Rolling Over Negative Equity Is Risky

Rolling negative equity into a new loan increases:

- Your total loan amount

- Your monthly payment

- The total interest paid over time

- The likelihood of remaining upside down longer

- The risk of repeating the negative equity cycle

If the replacement vehicle also depreciates quickly, you could find yourself carrying even greater negative equity on a car within a short period of time. When unpaid balances are rolled into a new auto loan, your starting principal increases immediately. This rollover effect widens the gap between your loan balance and your vehicle's market value, making it more difficult to rebuild equity and reduce long term borrowing costs.

When Trading In Might Still Make Sense

There are situations where trading in a vehicle with negative equity could be financially reasonable, such as:

- Your current vehicle has escalating repair costs

- You are moving to a significantly more affordable vehicle

- A lower interest rate meaningfully reduces long term borrowing costs

- You are restructuring debt to improve overall cash flow

- You are avoiding higher future depreciation risk

The key question is whether the new loan structure improves your financial position or simply postpones the problem.

Trading in a car with negative equity does not always make things worse, but it requires a careful review of your loan to value ratio, remaining balance, and total borrowing costs. Without a clear strategy, rolling debt into a new loan can increase long term interest payments and limit your flexibility to refinance or restructure your financing later.

Before trading in, review:

- Your current loan payoff amount

- Your vehicle's realistic market value

- The full principal amount of the new loan

- The interest rate and total interest paid over the new term

- Whether refinancing your current loan is a viable alternative

In many cases, keeping the vehicle longer, paying down the balance faster, or refinancing may be safer than rolling debt into a new loan.

How Can You Avoid Negative Equity on a Car in the Future?

Avoiding negative equity on a car begins with how you structure your auto financing from the start. While vehicle depreciation is unavoidable, your loan design plays a major role in managing risk. Factors such as your down payment amount, interest rate, loan term length, and total financed balance all determine whether your loan stays aligned with your vehicle's realistic market value over time.

Here are practical ways to reduce the risk of becoming upside down on a car loan:

1. Choose a Reasonable Loan Term

Shorter loan terms help you build equity faster because more of each payment goes toward principal. While longer terms reduce monthly payments, they slow principal reduction and increase the period during which your loan balance may exceed your vehicle's value.

2. Avoid Rolling Over Old Debt

If possible, resolve negative equity before purchasing another vehicle. Rolling unpaid balances into a new loan increases your principal from day one and raises the risk of repeating the negative equity cycle.

3. Be Selective With Financed Add-Ons

Extended warranties, protection packages, and service contracts can add thousands to your total loan amount when financed. Carefully evaluate whether financing these items aligns with your long term financial goals, especially when considering total interest paid over time.

4. Monitor Your Loan to Value Position Regularly

Periodically review your loan payoff amount and compare it to your vehicle's realistic market value. Tracking your loan to value ratio helps you identify potential equity gaps early, giving you time to adjust your repayment strategy before the imbalance grows.

5. Refinance Strategically When Appropriate

If interest rates decline or your credit profile improves, refinancing may help lower your rate and accelerate principal repayment. The objective is not only a lower monthly payment, but a loan structure that reduces total borrowing costs and shortens the time you remain exposed to negative equity on a car.

Negative equity on a car often develops from small financing choices that add up over time, such as taking longer loan terms, financing add ons, or rolling unpaid balances into a new loan. By planning your car finance agreement carefully and reviewing your loan structure regularly, you can keep your loan balance better aligned with your vehicle's market value.

Prevention is almost always more cost effective than trying to correct negative equity after it has grown.

Final Thoughts on Negative Equity on a Car

Negative equity on a car is more common than many drivers realize, especially in today's vehicle market. It occurs when your auto loan balance exceeds your vehicle's current market value, often because car depreciation outpaces principal repayment. Long term loans, high interest rates, rolling over debt, or financing add-ons can gradually create an upside down car loan over time.

The good news is that negative equity is manageable once you clearly understand your numbers. By reviewing your current loan payoff amount, estimating your vehicle's realistic resale or market value, and calculating your loan to value ratio, you gain a clearer picture of your position. With that information, you can make proactive, well planned decisions instead of reacting under financial pressure.

In some situations, keeping your vehicle longer and making additional principal payments may help close the equity gap. In others, refinancing your auto loan to secure a lower interest rate or better loan structure can improve cash flow and reduce total borrowing costs. If you are considering a trade in, understanding your equity position first is essential to avoid rolling debt forward unnecessarily.

What matters most is awareness and strategy. When you understand how negative equity develops, how to compare your loan payoff to your vehicle's value, and how to reduce the gap, you can make more confident financing decisions. Reviewing your numbers carefully today can help prevent larger financial strain and limited options in the future.

Frequently Asked Questions

What is negative equity on a car in simple terms?

Negative equity on a car means you owe more on your auto loan than your vehicle is currently worth. If your loan payoff amount exceeds the car's market value, the difference is your negative equity. This situation is often called being upside down on a car loan and can make selling, trading in, or refinancing more complicated.

How do I calculate negative equity on a car?

To calculate negative equity, subtract your vehicle's current market value from your loan payoff balance. If your payoff amount is higher than the vehicle value, the difference is your negative equity. For example, if you owe $20,000 and your car is worth $17,000, you have $3,000 in negative equity.

Can I refinance a car with negative equity?

Yes, refinancing a car with negative equity is sometimes possible, but it depends on your loan to value ratio, credit profile, and lender guidelines. If the gap between your loan balance and vehicle value is manageable, refinancing may help lower your interest rate or improve payment structure. If the gap is too large, options may be limited.

Is negative equity on a car bad?

Negative equity is not always a crisis, but it does limit your financial flexibility. It can limit your ability to trade in, sell, or restructure your loan without carrying forward debt. The longer the equity gap exists, the more interest you may pay over time. Managing it early reduces long term cost exposure.

How can I avoid negative equity on a car?

You can reduce the risk of negative equity by choosing a reasonable loan term, avoiding rolling over old debt, and limiting financed add-ons. Monitoring your loan balance and vehicle value regularly also helps you identify potential issues before they grow.

Does negative equity affect my credit score?

Negative equity itself does not directly affect your credit score. However, financial strain caused by high payments could increase the risk of missed or late payments, which would impact your credit. Maintaining consistent payment history is the most important factor for protecting your score.

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.