Last Updated: March 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: October 2024

By: Danielle Burton

Category: Leasing vs. Buying a Car, Auto Refinancing

Auto loan refinancing in Canada allows you to replace your current car loan with a new one that better fits your financial situation. When you refinance your loan, you may be able to lower your interest rate, reduce your monthly car payments, or adjust your loan duration to improve cash flow.

With an online platform like SafeLend Canada, you can explore refinancing options, complete a simple application process, and compare offers from different lenders in one place. Whether you have negative equity, positive equity, or credit issues, refinancing can help improve your financial health and support better financial decisions.

This guide explains how the refinancing process works, what impacts lender approval, and how factors like your credit report, credit scores, and income influence your loan application. By understanding your options, you can reduce interest charges and move closer to long-term financial freedom.

Key Takeaways

Auto loan refinancing can help lower interest charges, reduce monthly car payments, and improve your overall loan structure. Approval is based on factors like your credit report, credit scores, income, and current loan balance. With platforms like SafeLend Canada, you can compare refinancing options in one place, including solutions for borrowers with subprime loans. Making informed financial decisions can support long-term financial health and financial freedom.

In This Guide:

- 1. What Is Auto Loan Refinancing in Canada?

- 2. How Does Auto Loan Refinancing Work?

- 3. What Is the Auto Loan Refinance Process Step by Step?

- 4. How Can Auto Loan Refinancing Help You Save Money?

- 5. Should You Choose a Long-Term or Short-Term Auto Loan?

- 6. Can You Refinance a Car Loan with Bad Credit in Canada?

- 7. Frequently Asked Questions About Auto Loan Refinancing

What is Auto Loan Refinancing in Canada?

Auto loan refinancing in Canada means replacing your current car loan with a new loan from a financial institution that offers better terms. The new lender pays off your existing loan, and you continue making payments under a new loan agreement.

Through auto refinancing, borrowers often aim to reduce interest charges, improve loan duration, and better manage their monthly car payments based on their current financial situation.

Drivers typically refinance to:

- secure a lower interest rate

- reduce monthly car payments

- adjust loan duration to better fit their budget

Refinancing can help if your financial situation has improved, your credit score has increased, or you are working through past credit issues and want better options through a platform like SafeLend Canada.

Whether you have negative or positive equity, refinancing your auto loan can help improve your financial health, lower borrowing costs, and support better financial decisions.

How Does Auto Loan Refinancing Work?

Auto loan refinancing works by transferring your existing car loan to a new financial institution that offers improved terms. Instead of continuing with your current lender, a new lender pays off your remaining loan balance and replaces it with a new loan agreement.

The new loan is structured based on your current financial profile, which may include your credit score, income, outstanding debt, and the value of your vehicle. These factors determine your interest rate, loan term, and monthly payment.

Depending on your situation, refinancing can:

- lower your interest rate if your credit has improved

- reduce monthly payments by extending your loan term

- shorten your loan term to reduce total interest costs

Refinancing is often done through an online platform where you can compare options and submit one application instead of applying with each lender separately.

What Changes When You Refinance a Car Loan?

When you refinance, the following parts of your loan may change:

- your interest rate

- your monthly payment

- your loan term

- your lender

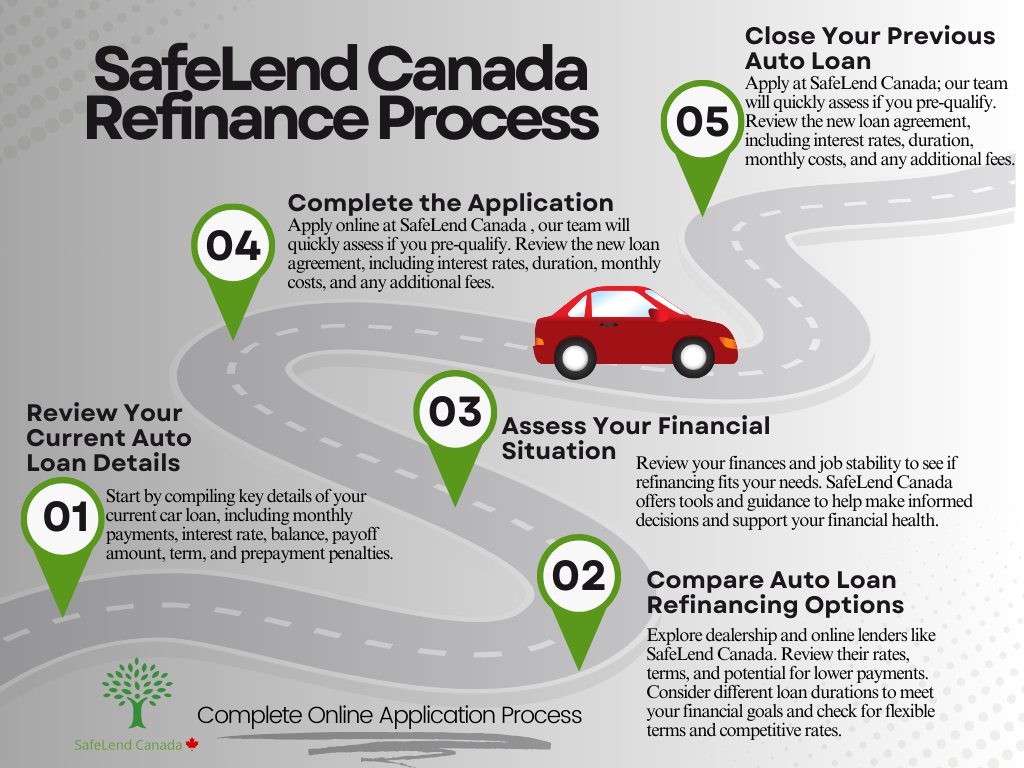

What Is the Auto Loan Refinance Process Step by Step?

Once you understand how auto loan refinancing works, the next step is following a structured process to secure better loan terms. From reviewing your current loan to submitting a refinance application and comparing offers from lenders, each stage plays a role in improving your financing outcome.

The auto loan refinance process typically involves 5 to 7 steps, depending on the lender and your financial situation.

1. Review Your Current Auto Loan

Start by looking at your existing loan details, including your remaining balance, interest rate, monthly payments, and loan term. This helps determine whether refinancing will reduce your costs or improve your loan structure.

2. Assess Your Credit and Financial Situation

Lenders evaluate your credit score, income, and overall financial stability when reviewing your refinance application. If your credit or income has improved since your original loan application, you may qualify for better financing options.

3. Compare Financing Options from Lenders

Use an online platform or work directly with a financial institution to compare available loan offers. Reviewing multiple options helps you identify competitive interest rates, flexible terms, and the best overall loan structure.

4. Submit Your Refinance Application

Complete a refinance application by providing your personal, financial, and vehicle details. Many platforms allow you to submit one loan application and receive multiple offers, simplifying the process.

5. Review and Select the Best Loan Offer

Carefully evaluate each offer, including the interest rate, loan term, monthly payment, and total cost of borrowing. Focus on the full financial picture rather than just lowering your monthly payment.

6. Finalize the New Loan and Pay Off the Existing One

Once you accept a new loan, the lender pays off your current auto loan. You then begin making payments under the new loan agreement, ideally with improved terms and better financial alignment.

Following a structured refinance process can help you reduce interest costs, improve cash flow, and choose financing options that better match your current financial goals.

How Can Auto Loan Refinancing Help You Save Money?

Auto loan refinancing can help reduce the overall cost of your loan by improving your interest rate, adjusting your loan terms, or restructuring your payments. When done strategically, it can create both immediate monthly savings and long-term financial benefits.

1. Lower Your Interest Rate

If your credit score or financial profile has improved since your original loan application, you may qualify for a lower interest rate. Even a small reduction can lead to significant savings over the life of your loan.

2. Reduce Monthly Payments

Refinancing can lower your monthly payments by securing better terms or extending your loan duration. This can improve cash flow and make your payments more manageable within your budget.

3. Reduce the Total Cost of Borrowing

Choosing a shorter loan term or a lower interest rate can decrease the total amount of interest paid over time, helping you save money in the long run.

4. Adjust Your Loan to Fit Your Current Financial Situation

Refinancing allows you to restructure your loan based on your current needs. This could include changing your loan term, removing a co-signer, or aligning payments with your income.

5. Access Better Financing Options

Using an online platform or working with multiple lenders allows you to compare financing options and select a loan that better fits your financial goals.

By improving your loan structure, refinancing can help you better manage debt, reduce financial stress, and make more informed financial decisions.

Should You Choose a Long-Term or Short-Term Auto Loan?

When refinancing your auto loan, choosing the right loan term is one of the most important decisions. A shorter or longer term will directly impact your monthly payments and the total cost of your loan.

Short-Term Auto Loans

Short-term loans typically come with higher monthly payments but lower total interest costs.

Best for:

- reducing the total cost of borrowing

- paying off your loan faster

- borrowers with stable income and room in their budget

Long-Term Auto Loans

Long-term loans offer lower monthly payments but usually result in higher total interest over time.

Best for:

- improving monthly cash flow

- managing tight budgets

- reducing immediate financial pressure

Key Factors to Consider

Before choosing your loan term, consider:

- Monthly budget: Can you comfortably afford higher payments?

- Total loan cost: Longer terms increase total interest paid

- Financial goals: Do you want to reduce debt faster or improve cash flow?

- Current loan balance: This may affect available refinancing options

Which Loan Term Saves You More Money?

In most cases, shorter loan terms save more money overall due to lower interest costs, while longer terms provide more flexibility with lower monthly payments.

The right loan term depends on your financial priorities, whether that is lowering monthly payments or minimizing the total cost of your loan.

Can You Refinance a Car Loan with Bad Credit in Canada?

Yes, it is possible to refinance a car loan with bad credit in Canada. While your credit score matters, lenders also look at your income, payment history, and overall financial stability when reviewing your application.

What Lenders Look At Beyond Your Credit Score

Even with a lower credit score, lenders may approve your loan application based on:

- Income stability: Consistent income improves your ability to qualify

- Payment history: Recent on-time payments can strengthen your application

- Debt levels: Lower overall debt can improve your approval chances

- Vehicle value: Helps determine your equity position

When Refinancing with Bad Credit Makes Sense

Refinancing may still be a good option if:

- your financial situation has improved since your original loan

- you are currently dealing with high interest rates

- you need to reduce your monthly payments for better cash flow

- you want to restructure your loan to better match your budget

What to Expect When Refinancing with Bad Credit

- Interest rates may be higher than prime borrowers

- Loan terms may be adjusted to manage risk

- Approval may depend more on income and payment history than credit score alone

Can You Get a Lower Interest Rate with Bad Credit?

In some cases, yes. If your financial situation has improved or your previous loan carried very high interest, refinancing could still result in better terms.

Even with bad credit, refinancing can be a useful strategy to improve loan structure and manage your financial obligations more effectively.

Final Thoughts on Auto Loan Refinancing in Canada

Auto loan refinancing in Canada can be an effective way to lower your interest rate, reduce monthly car payments, and improve your overall loan structure. When you refinance your loan, reviewing your current loan, comparing refinancing options, and aligning your loan duration with your financial goals can help reduce interest charges and create both short-term relief and long-term savings.

Whether you are dealing with negative equity, credit problems, or improving your credit score, refinancing can help you adjust your auto loan and support your financial health. Using an online platform like SafeLend Canada makes the application process and refinancing process easier by connecting you with multiple lenders, increasing your chances of approval, and allowing you to compare loan offers in one place.

Before moving forward, review your credit report, loan details, and budget to make sure your new loan supports smart financial decisions and helps you reach long-term financial freedom.

Frequently Asked Questions About Auto Loan Refinancing

What is auto loan refinancing?

Auto loan refinancing means replacing your current car loan with a new loan that offers better terms, such as a lower interest rate, different loan term, or reduced monthly payments.

How can auto loan refinancing help you save money?

Refinancing can lower your interest rate, reduce monthly payments, or shorten your loan term, which can decrease the total cost of borrowing over time.

Can I refinance a car loan with bad credit in Canada?

Yes, refinancing is possible with bad credit. Lenders may consider your income, payment history, and overall financial stability in addition to your credit score.

What do you need to refinance a car loan?

You typically need proof of income, identification, vehicle details, and your current loan information to complete a refinance application.

How do I start the auto loan refinancing process?

Start by reviewing your current loan, checking your financial situation, and submitting a refinance application through a lender or online platform to compare financing options.

Does refinancing a car loan affect your credit score?

A refinance application may involve a credit check, which can cause a small temporary impact. However, successful refinancing and consistent payments can help improve your credit over time.

When is the best time to refinance a car loan?

The best time to refinance is when your credit score has improved, interest rates have dropped, or your financial situation has changed.

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.